Following are my personal comments on specific markets and issues. I chart markets for a hobby and my comments are the result. They are not recommendations to buy or sell anything and should not be thought of as such. They are for entertainment purposes only so enjoy.

Please remember, the following is pure speculation based only on my experience and chart patterns. "Every sunken ship has a room full of charts."

David Bruce Edwards

Aug. 1, 2026

Note - I got a new, wider screen monitor and when I look at this web site with the screen size in full, the site spacing does not come out properly. By making the window less wide all of the text and graphics slide into place. Perhaps you are having the same experience. DBE.

As usual, I will show pictures and graphs found on Zerohedge.com, Sentimentrader.com, which include the Seasonality charts and charts made on Barchart.com. I will also mention "cycle low timing bands" suggested by another market website to which I subscribe, Cyclesman.com.

The three biggest events in markets over the last two weeks were: 1. The Fed decision to leave overnight borrowing rates unchanged. 2. Ups and Downs in oil and refined products due to both wars. 3. The spectacular crash and bounce in semiconductor stocks.

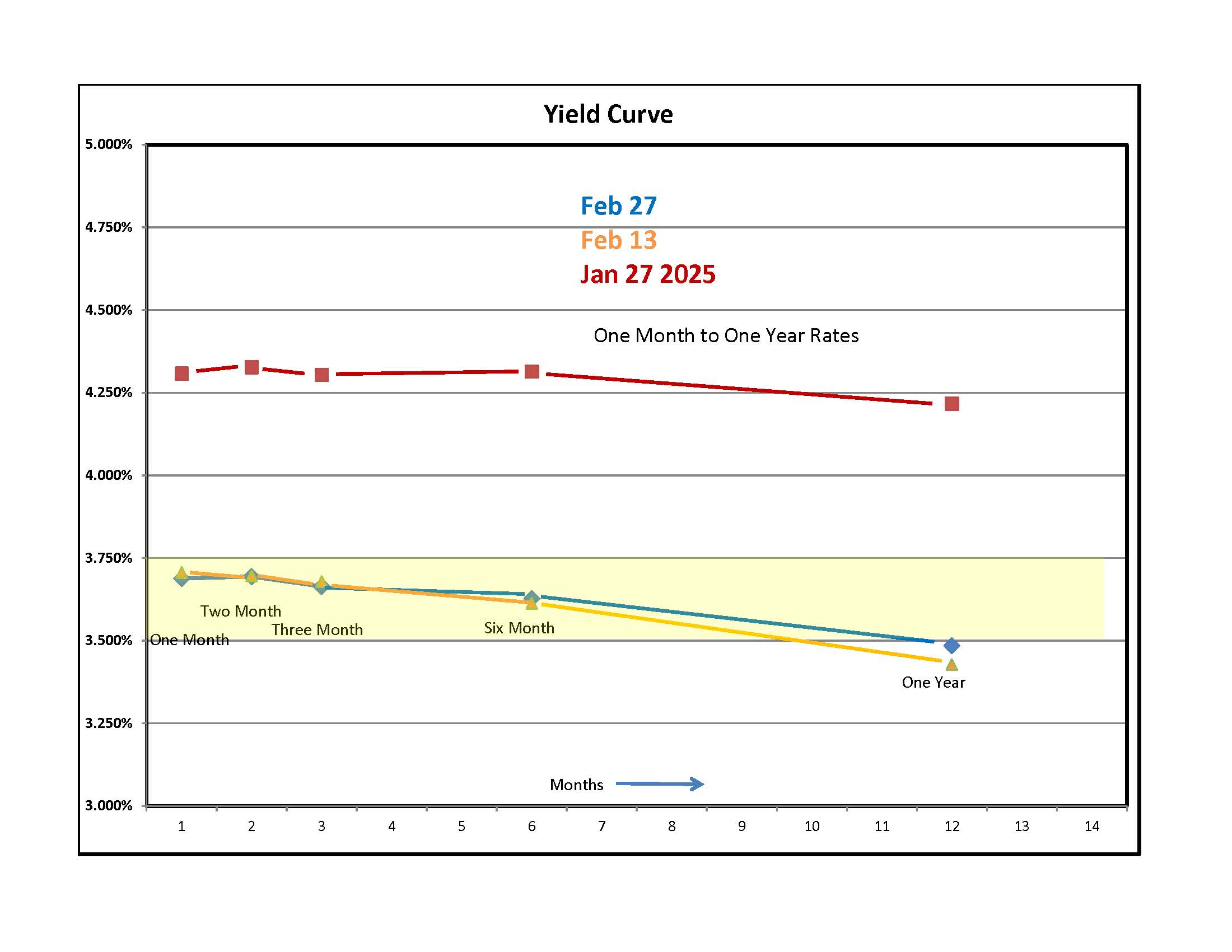

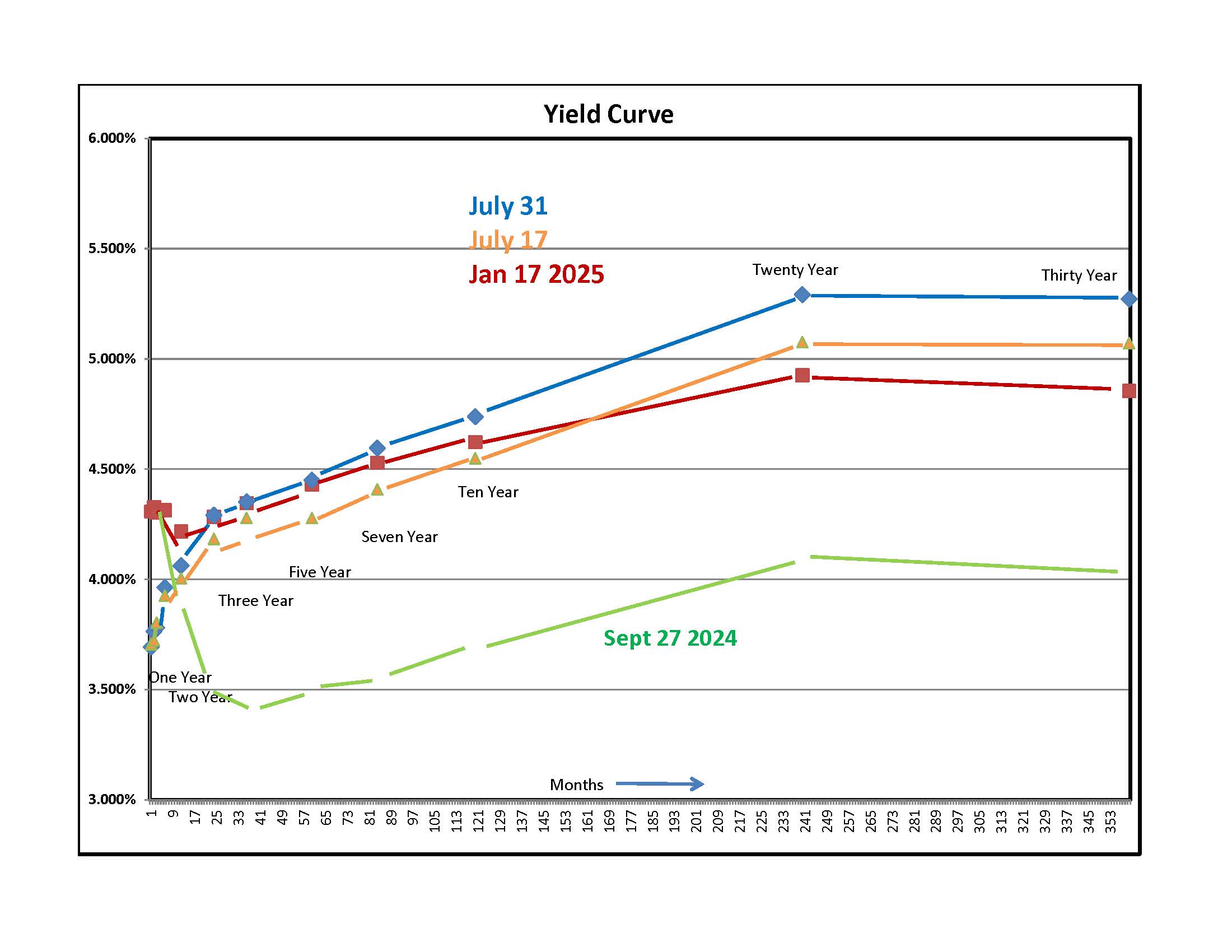

On Wednesday, the Fed left overnight lending rates to banks unchanged. The yellow area on the left side graph highlights the Fed Funds target rate. The market expected a hike because in past cycles, when rates on the shorter end of the curve traded above the Fed Funds band, they raised. The quick market reaction was for rates on the very short end of the curve to fall slightly and for everything farther out to rise. The blue lines on both graphs show Friday's curve. The reasoning was that inflation is above the Fed's two percent target range and the Fed is not doing enough to bring it down. Fan's of Fed Chairman Kevin Warsh point out that the bond market is already doing the Fed's work with rates edging higher over the last few months in response to robust economic indicators. A few decades ago, inflation and deflation had to do with banks increasing and decreasing lending to businesses. The Fed raised rates when they thought the economy was running hot. After a hike, banks raised their lending rates and returns to businesses on borrowed money were less attractive. In 2026, inflation is the result of the demand for things fueled by capital expenditures for data centers, targeted government spending for critical materials and defense and transfer payments such as social security, medicare and medicaid, food stamps (SNAP) and other government programs that account for an estimated 30% of consumption. Raising overnight lending rates to banks will not affect these sources of inflation. The government spending is inelastic to Fed policy shifts. Rates have been rising for four years and Google, Microsoft, Meta, SpaceX and Oracle keep borrowing and pumping money into the economy. Most government borrowing is on the short end of the curve so raising rates would increase the interest rate debt burden on the Treasury. Small businesses that borrow on the left side of the curve would also be hurt. My guess is that Kevin Warsh thinks that AI CapEx spending is peaking and with it, price pressures on everything that goes into building data centers. He could also believe that the accelerated expensing provision in the Big Beautiful Bill encouraged businesses to buy things this year, pulling demand forward with suppliers raising prices. Once these two sources of demand run their course, inflation will subside and we could be looking at deflation.

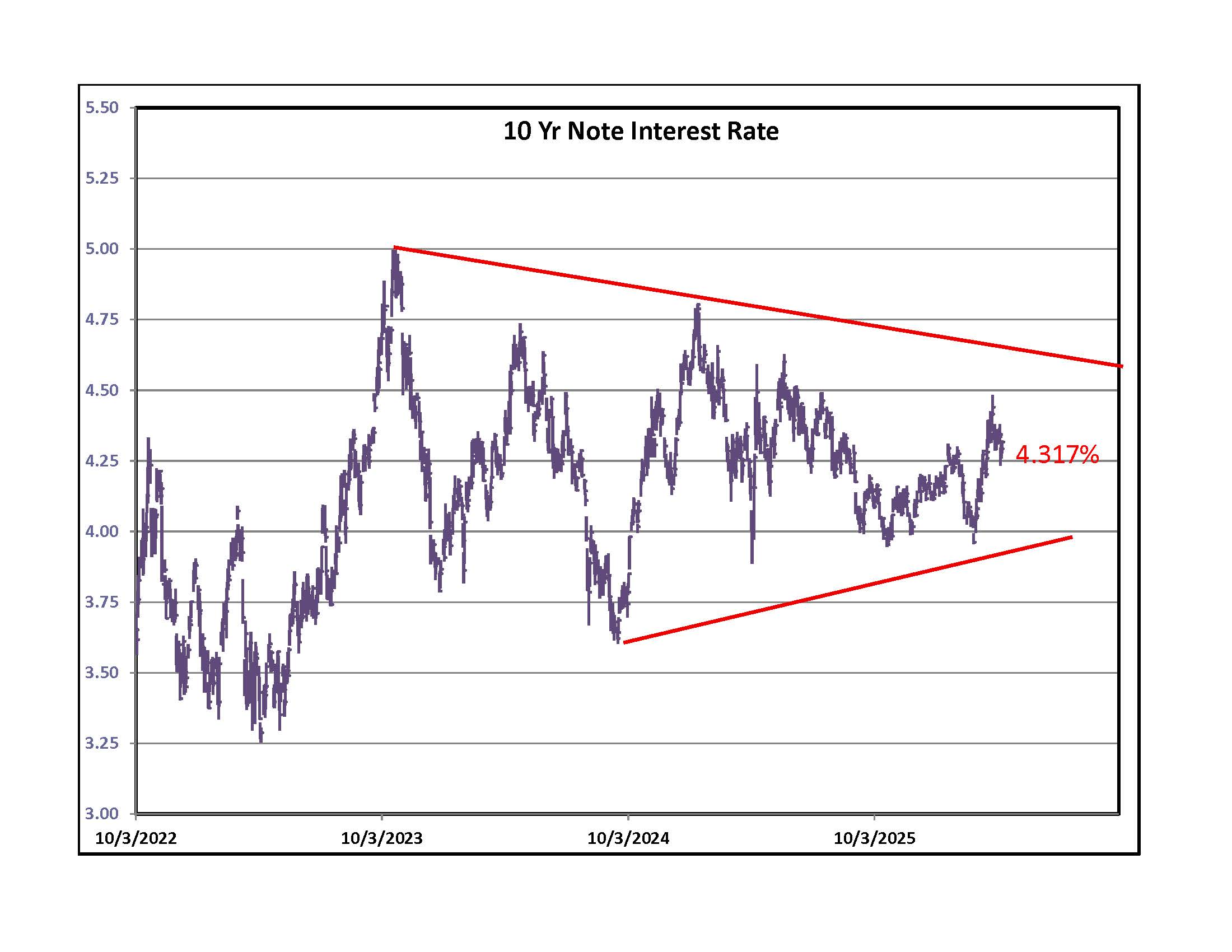

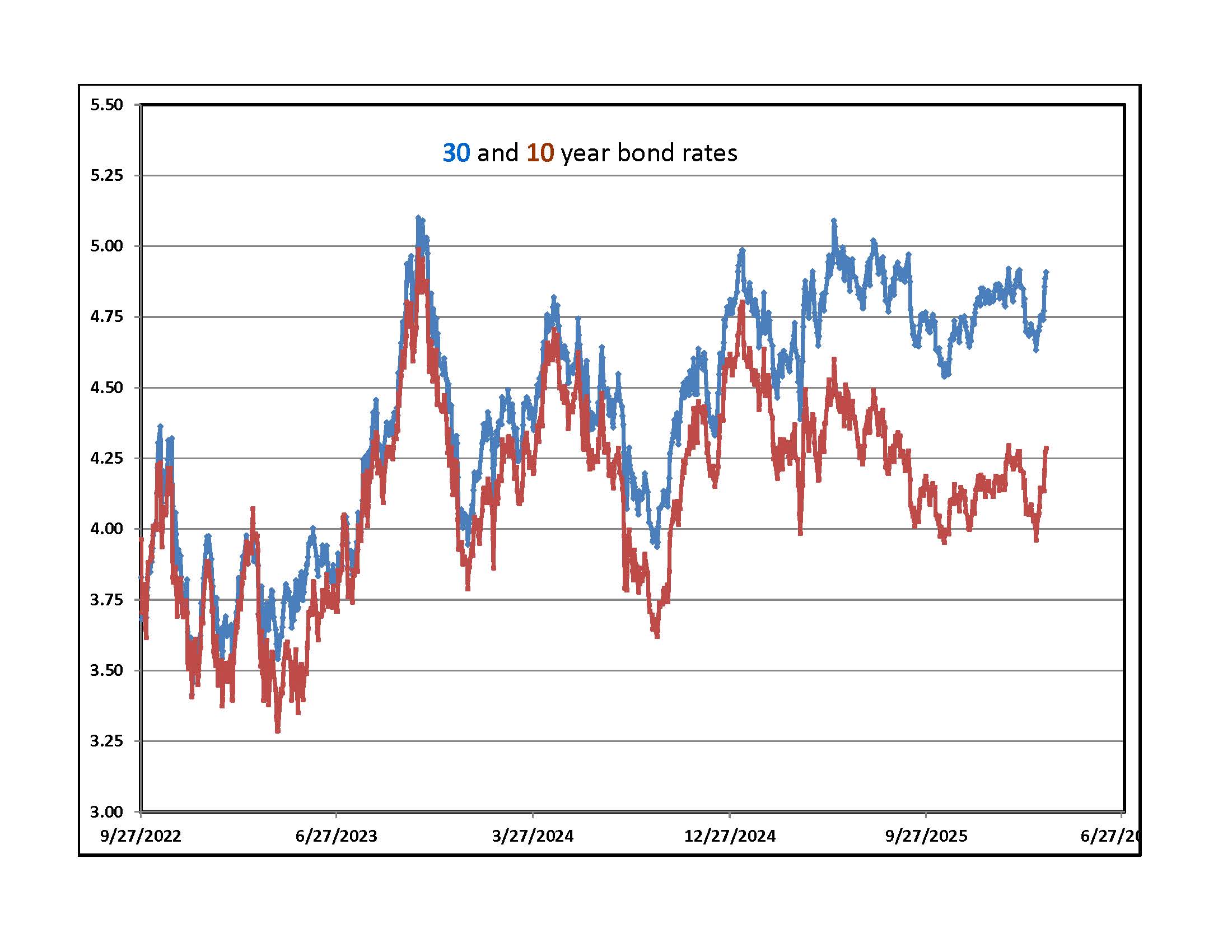

Rates on the 10 year note are challenging previous highs. Mortgage rates trade off of the 10 year so this is bad news for home buyers. Rates on our longest dated bonds are at a new high for the cycle, trading at around 5.27%. With shorter term rates unchanged or rising slightly and longer dated yields running higher, the carry trade is more profitable. Hedge funds borrow on the short end, paying rates shown on the left side of the yield curve graph and buy longer dated bonds on the right end of the curve. They lock in a spread between the rate they pay and the rate paid to them through ownership of longer dated bonds. When the market senses that rates have stabilized, watch for carry trade players to be big buyers of 30 year bonds, pulling their yield back down. Despite all the hand wringing over rates, the S&P 500 is around 2% below its all time high from June 2nd. Investors don't believe that rising rates will harm profits.

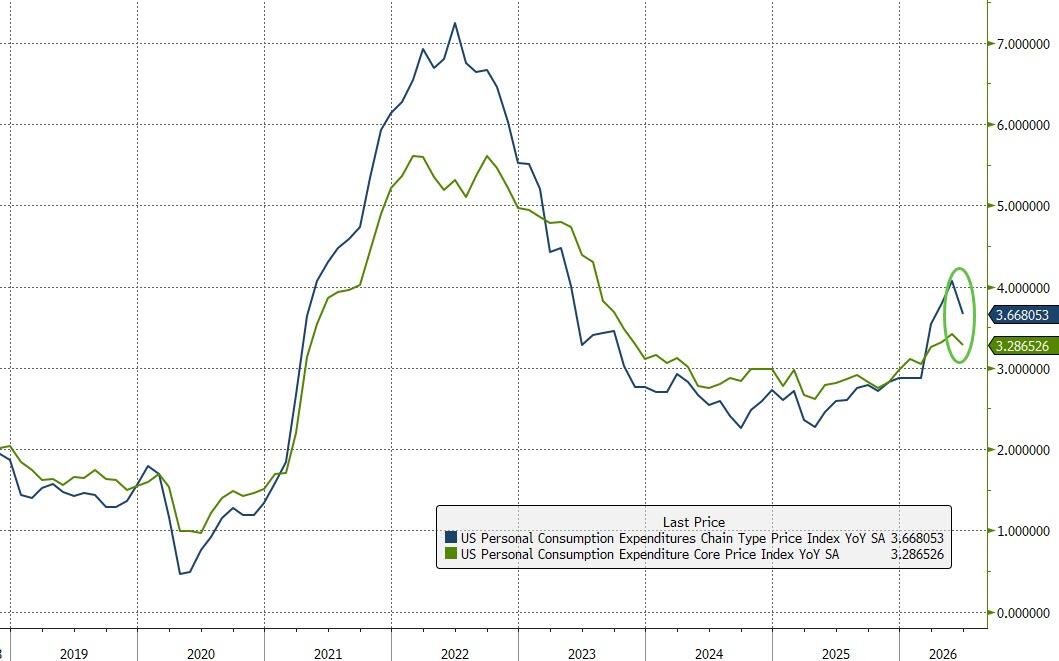

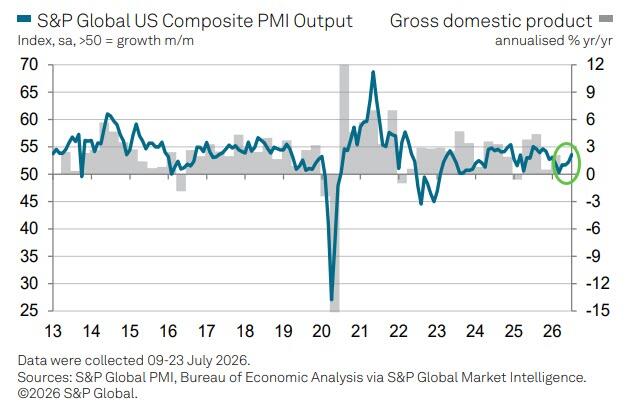

On the left is last week's Personal Consumption Index. The blue line includes food and energy costs. The green line subtracts those two items. The data came from June when oil prices were down so the headline number fell 0.1%, its first negative reading since the COVID scare in April of 2020. The Core reading rose only 0.1% leaving its annual rate of change at 3.3%, down from 3.4%. The increased cost of services were responsible for the gain. On the right is a graph showing the results from purchasing managers surveys on the outlook for their companies (blue line). The gray shaded area tracks quarterly GDP readings. The two tend to move together which implies strong growth for the third quarter.

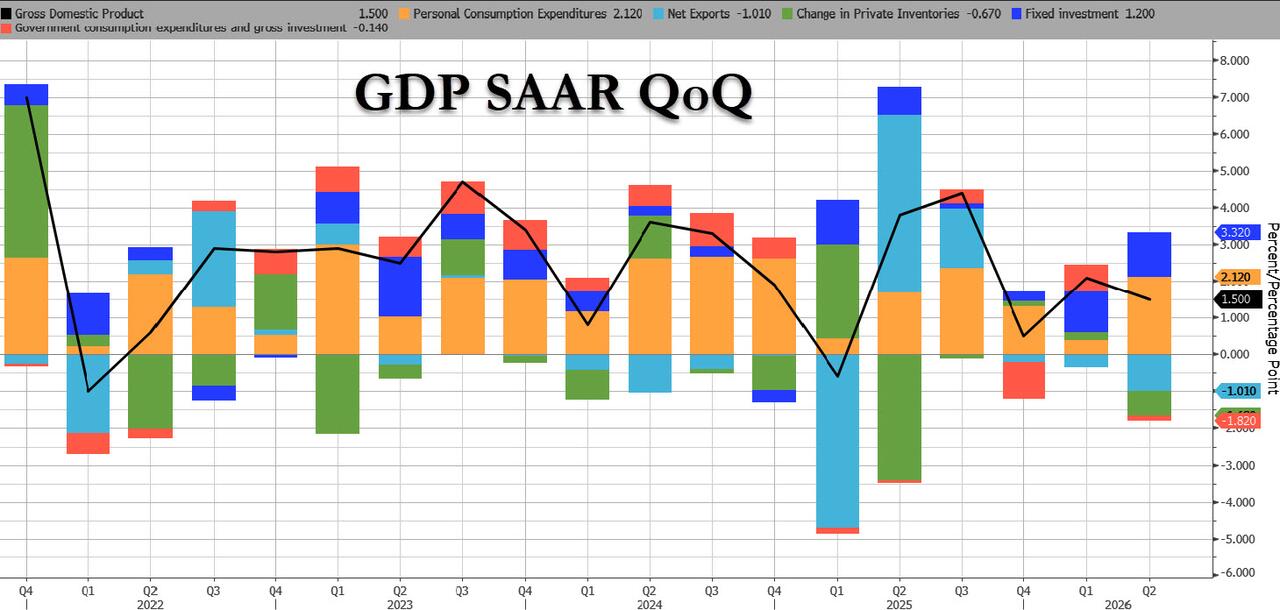

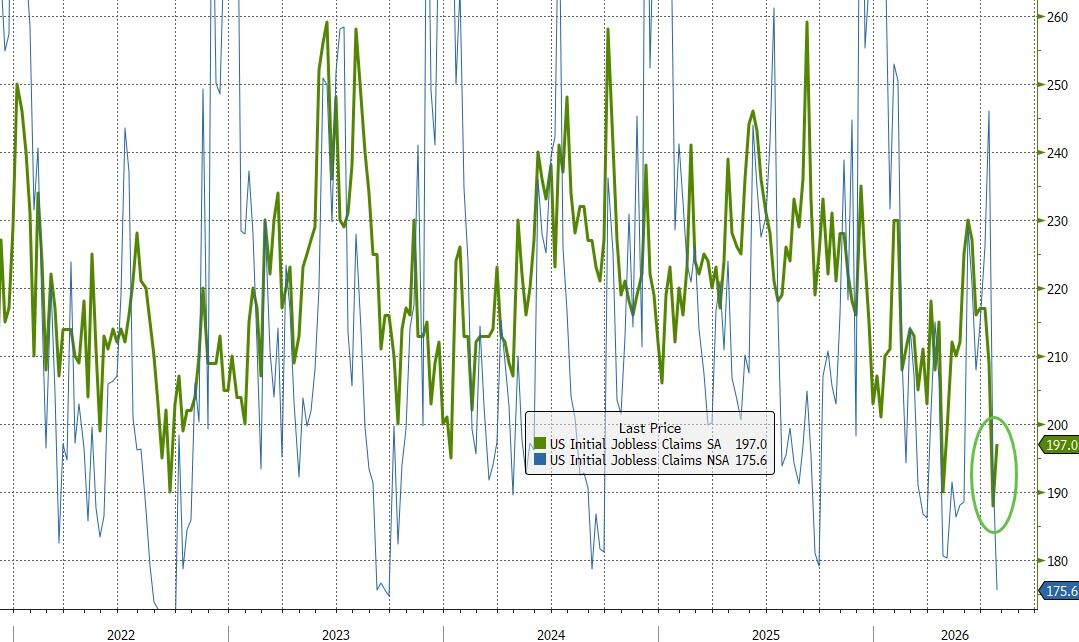

The left side chart shows details of the latest estimate of growth in the second quarter. Adjusted for inflation, it came in at 1.5%, below the Street's 2% estimate and far below what buyers of stocks anticipated. Personal Consumption (light orange) was strong and so was fixed investment (data centers for instance). The drag came from an increase in imports which is subtracted from GDP, lower government spending and lower business inventories. The right side graph shows the latest on New Claims for Unemployment Benefits. The number came in at 197,000 and the week before it hit 187,000, the lowest in 57 years. Despite all the worries over AI sparking massive job losses, there is no sign of it in the Claims data.

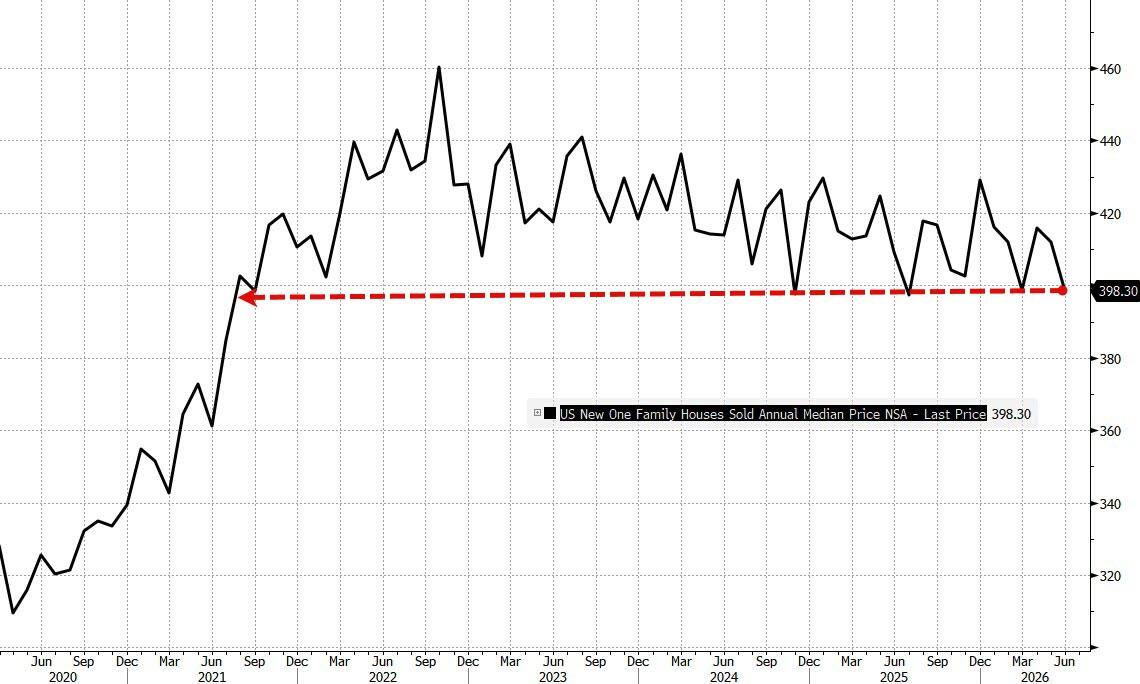

New Home Sales rose slightly (left side, green line) for the month. The median price (right side) fell to $398,300, back to levels seen right after COVID. New homes have to compete with existing homes and the inventory of existing homes for sale is growing steadily. I live in Boston's North Shore which has been one of the country's hottest markets for the last couple of years. In 2024, you could drive through neighborhoods and not see a For Sale sign. Now, they are common and the number of transactions is double what it was a year ago.

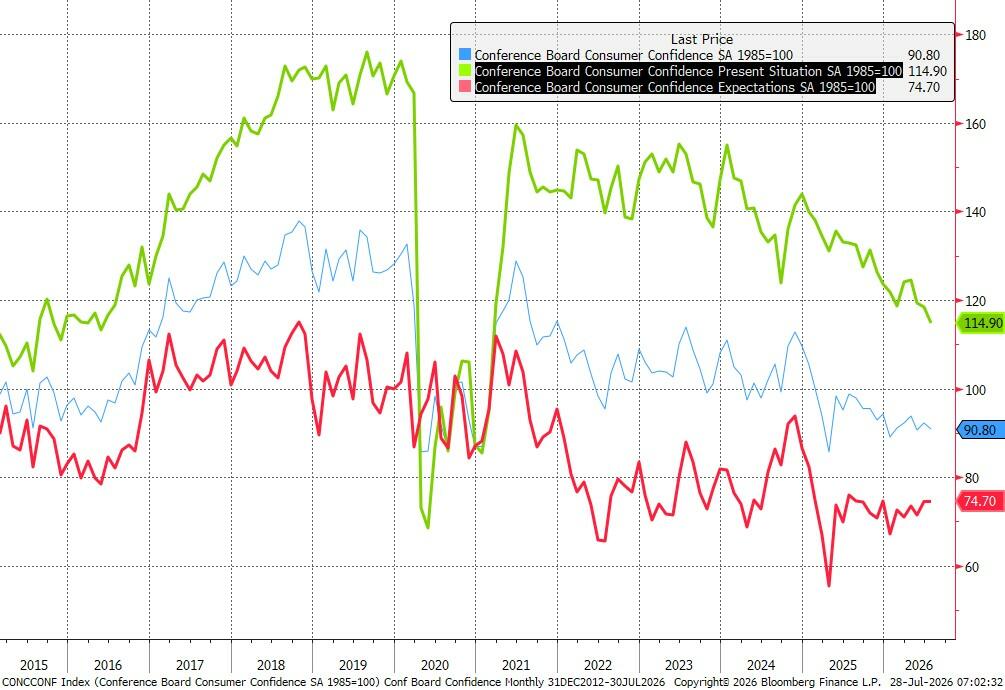

A Conference Board survey of economic conditions dropped slightly (left side, blue line) with respondents feelings about their current condition falling the most as shown by the green line. What is surprising is that the number one factor was unease over the job market, despite record low layoffs. Workers still suspect that bad news is due. They think that general business conditions will be unchanged in the future (red).

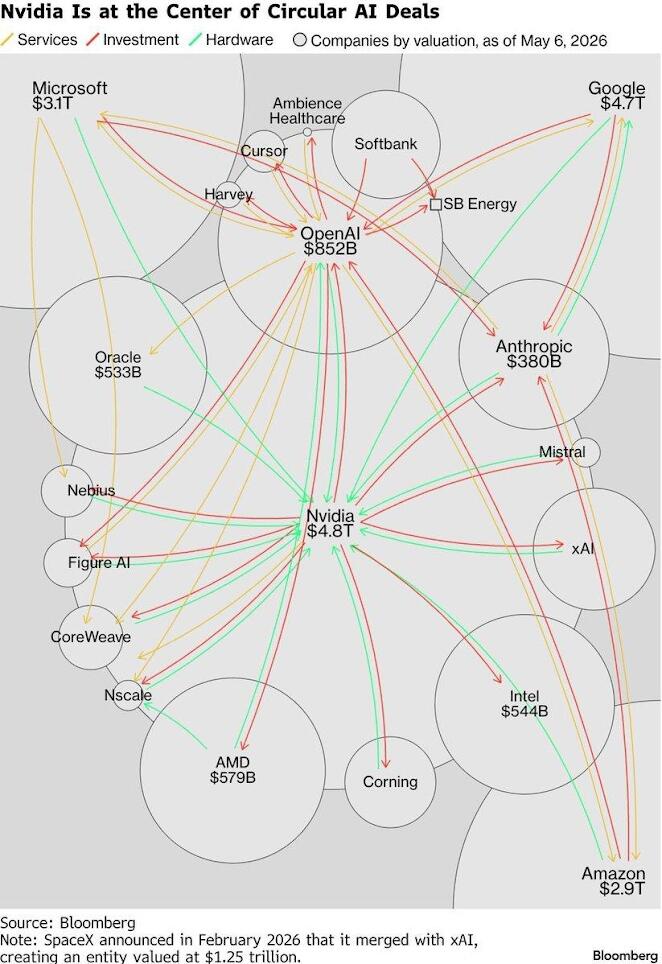

Over the last few weeks we saw a big sell off in AI related names, especially memory chips. Micron hit $1,255 on June 25th and fell to $705.04 on July 29th before rebounding. Investors are worried that bets in data centers will not pay off and that many of them will not be completed. Analysts are also worried that Nvidia is at the center of a circular financing scheme where they take their massive profits and invest in buyers of their chips to keep demand for their high priced hardware strong. The details of who is sending money to who and how much is murky. The graph to the right is one of the best illustrations. The unanswered question is, how will these companies ever recover the billions they are investing in AI? Last week there were more articles on Chinese models that cost a fraction of what Open AI and Anthropic want to charge. They are just as good or better at doing most tasks. Open AI slashed the price on one of their cheaper models to compete with China.

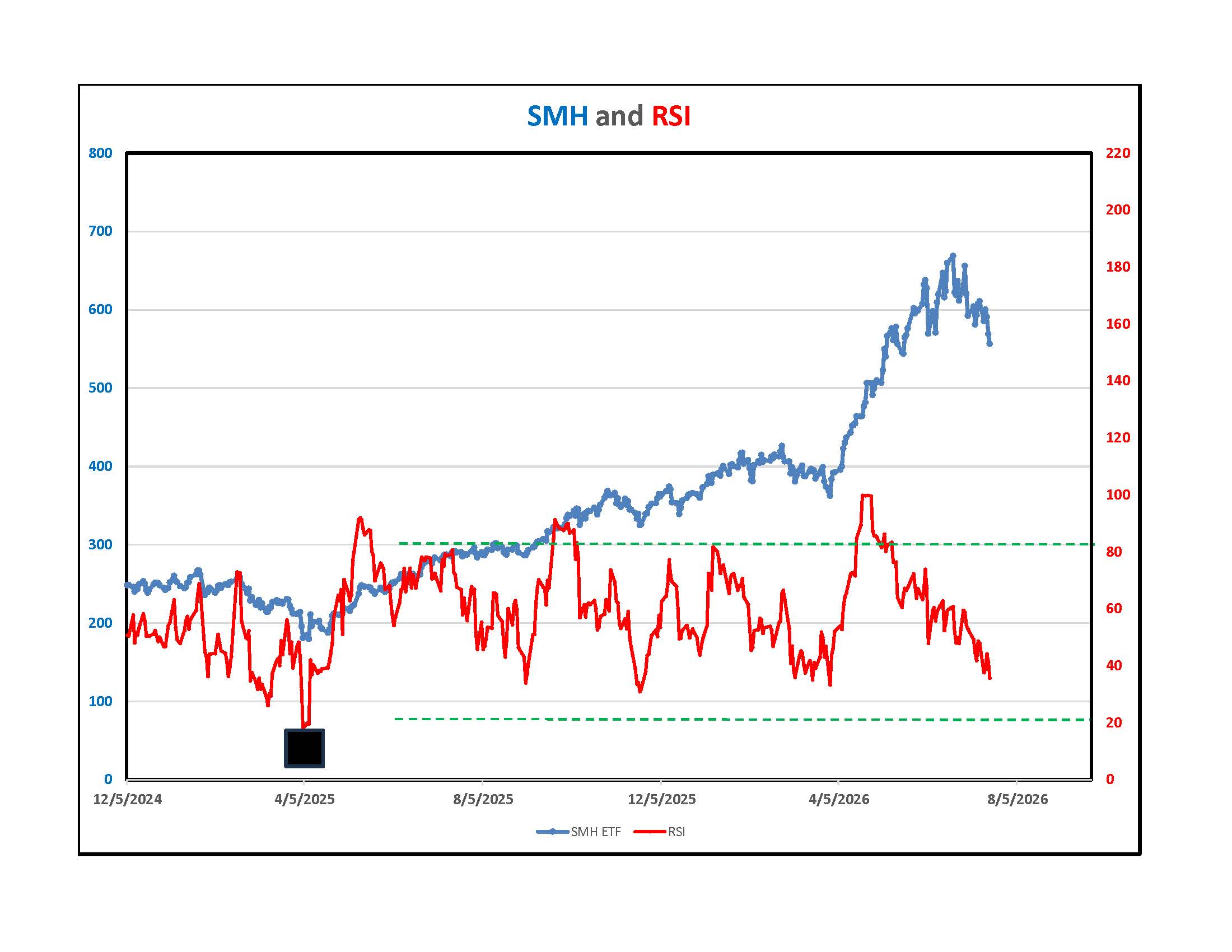

SMH is the popular ETF focused on computer chips. At times, the professional trading community acts like a pack of sharks. Last week, stories circulated about Leopold Aschenbrenner, a 24 year old genius who convinced investors to give him a billion dollars to invest in AI. His fund was called Situational Awareness. He loaded up on computer chip stocks and as they went higher, he borrowed against the increase value to buy more and more. Some reports say that he hit a high of around $45 billion dollars in value using four-to-one leverage. A few weeks ago, hedge funds smelled blood in the water and started selling the same set of stocks. Margin calls hit Situational Awareness and Leopold was forced to liquidate. His selling into a market where informed investors were standing aside, meant that the stocks collapsed forcing more margin calls and liquidations. By Thursday of last week he was wiped out. At that point, funds stepped in and bought chip stocks at prices last seen a couple of months ago. Thursdays reversal is being called the Leopold low. Above and to the left is a graph of SMH and a simple RSI oscillator in red. The black box is below a point in time when the RSI oscillator fell below 0.20. Despite intense selling last week, it didn't hit that point. My guess is that it will over the next month and that is when these stocks could be interesting again. Traders in Korea did the same thing as Mr. Aschenbrenner and when the dust settles, there will be more funds that report losses.

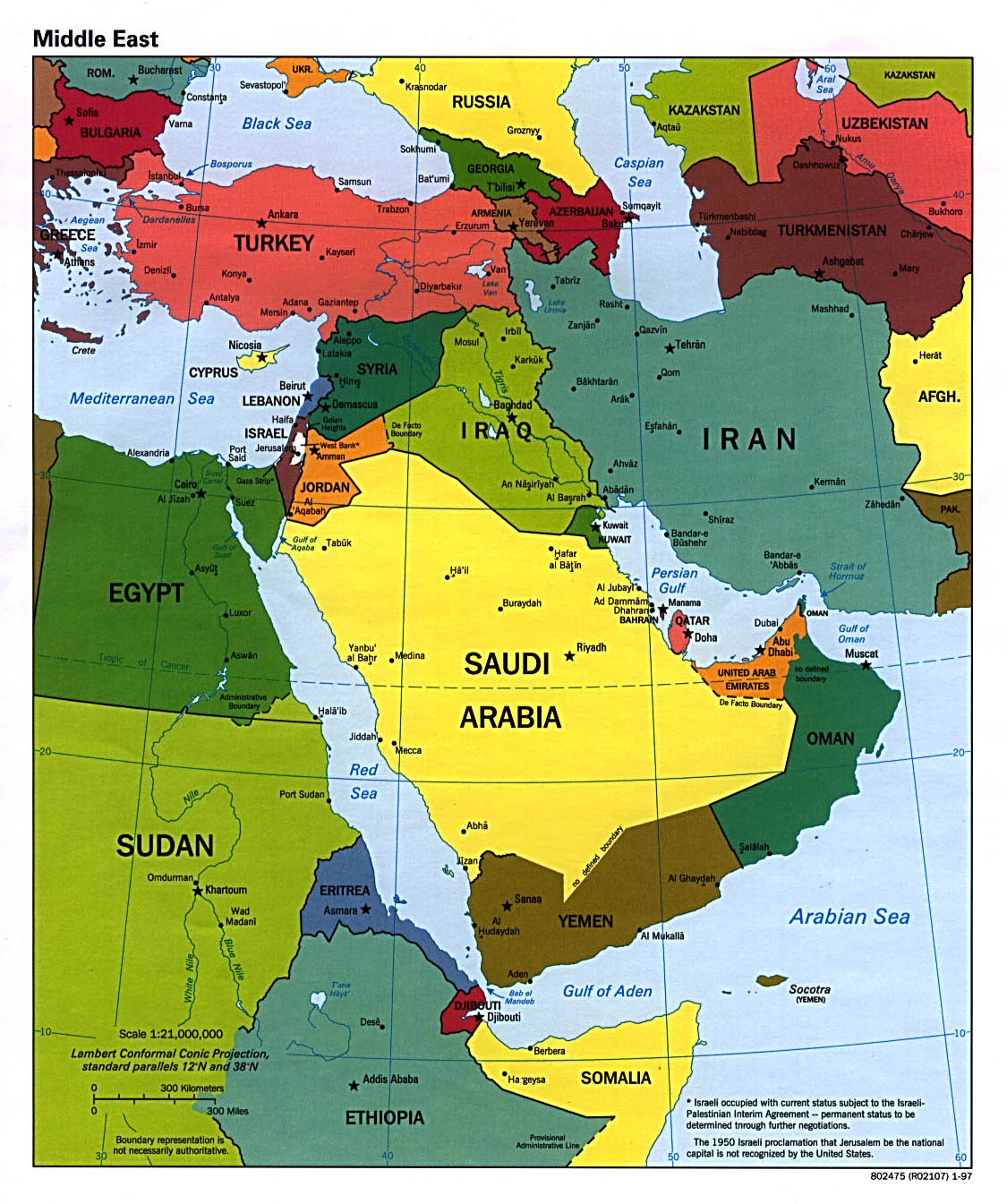

On Friday, there were reports that President Trump ordered heavy attacks on Iran, including their energy infrastructure. As of early Saturday morning, there is nothing to report. Traffic through the Strait is limited. Iran hit two tankers and U.S. bases. They also got the Houthis to go after Saudi tankers filled with oil from a pipeline that skirts the Strait, exiting through the Bab el-Mandeb Strait on the Red Sea. One reason that oil prices were contained recently was this Saudi work around for getting oil to consumers. News outlets claim that Saudi Arabia is going to invade Yemen by ground and sea. There are also reports that the UAE has ground forces inside Iran.

In the last few decades, proposals were put forth for pipelines that would avoid both Straits. When oil prices were down, the economics of these plans didn't look good. Now, everyone is working on them. Think of the groups that Iran is funding. Hezbollah has a strong presence in Lebanon. They are an international criminal gang, making money from drugs and human trafficking with a well trained military. Hamas was in Gaza and the Houthis control parts of Yemen. Our perspective is that they are religiously inspired and hate Israel. Iran supports them because they are fellow Shia Muslims.

There is another way to think about Iran and its proxy groups. Iran wants to control the flow of oil from the Middle East. They back these other groups because they can use them as enforcers to block alternative shipping routes and pipelines for Middle East oil to get to the rest of the world. One proposed pipeline would start at Aqabah, at the lower left corner of Jordan and cross Gaza to the Mediterranean Sea. This was out of the question as long as Hamas controlled Gaza. Now, it can be considered. Some pundits claim that this was the real reason for Israel pushing residents into southern Gaza. There is a disarmament deal on the table with Hamas but this only includes heavy weapons and is contingent on Israel withdrawing from part of the Gaza Strip. Hamas or other players can still be paid to disrupt pipeline plans. The Houthis stop oil exiting the Red Sea and Hezbollah (and Shia militias) stop west bound pipeline plans that exit on the coast of Lebanon and Syria or go across Iraq and Syria and on to Turkey. If Iran succeeds, it will control 30% of the world's oil plus all the other things that go through the Strait of Hormuz. They can enrich themselves with tolls and demand all sorts of special treatment from the Asian countries that depend on oil from the region. They will become one of the most powerful countries in the world. They are not likely to give up on this vision and any agreement that is forced on them will be temporary. The only thing stopping their regional control is Israel which has enough military strength to wound their auxiliary police forces as we saw with Hamas and Hezbollah. Many conflicts that appear to be religious are actually about money and power.

On May 29th of 1453, Constantinople fell to Mehmed II. At the time, it was the capital of the Eastern Roman Empire and a gateway to trade with India and the Silk Road from China, the industrial powers of the day, producing premium goods that were sought by Europeans. With control of both sides of the Bosphorus and Dardanelles Straits, they could control trade and impose tariffs on everything going between the Black Sea and the Mediterranean. A century later, Europe was looking in another direction, toward the New World. Control of things in the East was less important. Today, Turkey charges $5.83 per net ton of cargo for transit through its Straits. The cost of stopping Iran may prove to be too hard to bear but as in the 1400s, the answer will be the development of oil and natural gas fields outside of this map. We are already seeing this and with the current high prices, exploration and development are going on everywhere. Refineries are custom built for particular blends of crude so Asian countries will be locked into dealing with Iran until they can modify their plants to take other feeds. Over time, Iran's grip on the Strait will decline in value and influence.

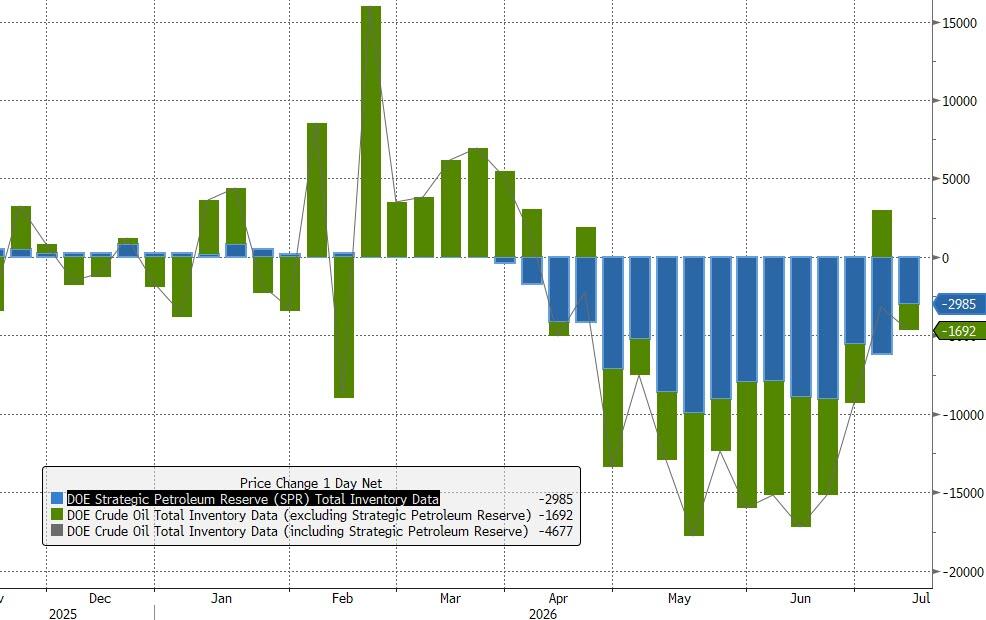

Domestically, oil inventories aside from the Strategic Reserve are at levels that are approximately 7% below the five year average for this time of the year so there is no shortage. Gasoline is 6% below and Distillates are 9% below. Prices for gasoline and diesel are high relative to oil because Ukraine is taking out Russian oil refineries. These plants made enough gas and diesel to supply Russia and export even more to the rest of the world. Due to Ukraine, exports stopped and traders are focusing on supplies from the U.S.

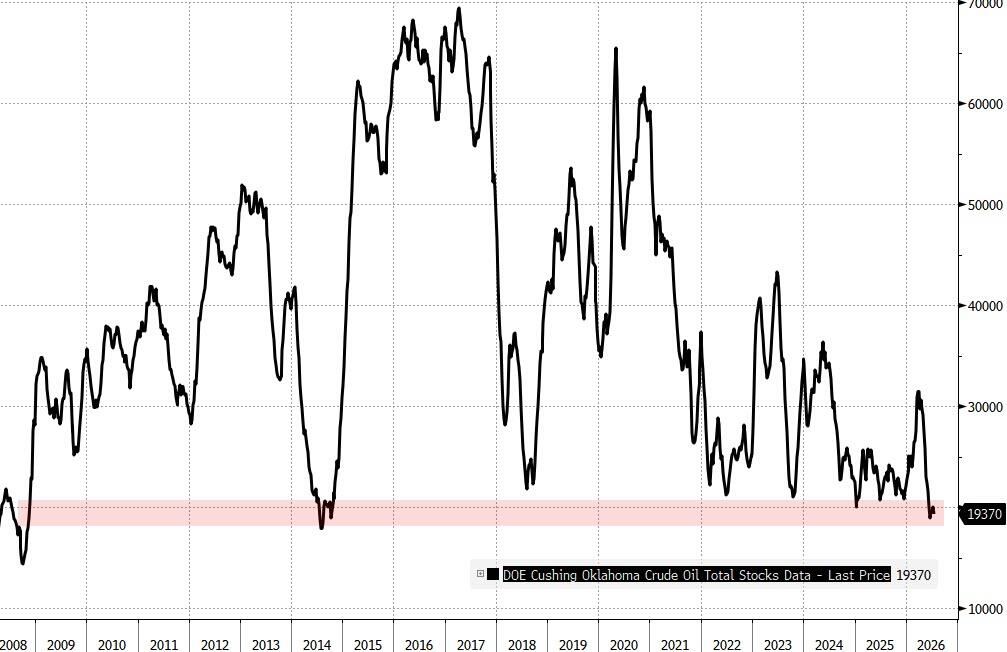

Oil refineries operated at 97.2% of their capacity, an extremely high rate. In September, fall maintenance season starts and this number will drop. On the upper left is a graph of the amount of oil stored at the nation's largest private crude oil storage hub in Cushing, Oklahoma. It is nearly at tank bottoms. On the right is a graph of the weekly additions or draw-down in inventories, including the Strategic Reserve which is shown in blue. The most recent weekly withdrawal from the reserve was 3,797,000 barrels. U.S. production is at around 13.7 million barrels per day, near record levels.

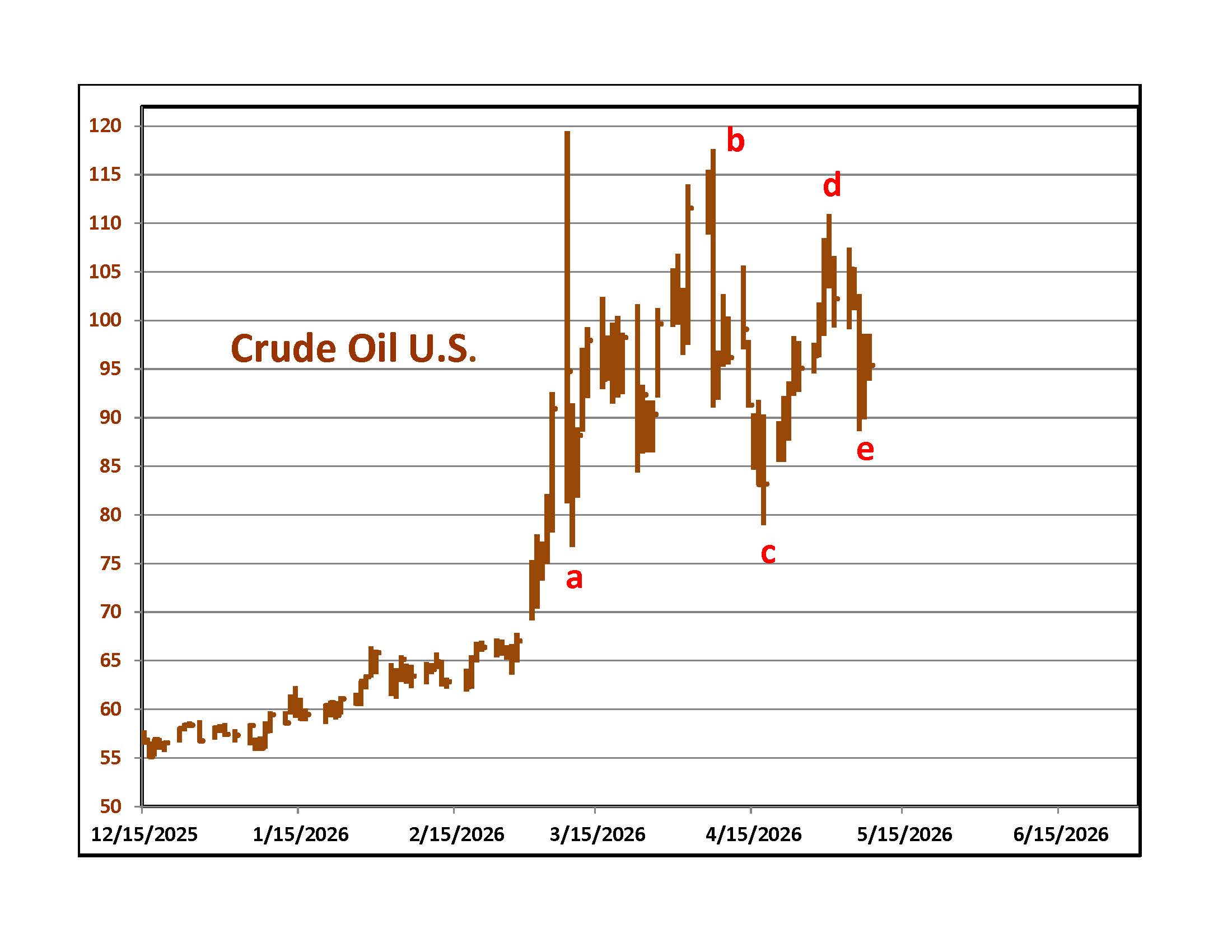

To the right is XLE, the big energy ETF dominated by Exxon and Chevron. No one knows what will happen in the middle east. Chart wonks will notice that XLE had an initial down move and is tracing out a text book "3,3,5" upward correction. The "3" parts are labeled a,b,c. If reality follows art, we have some good news that will complete wave 4 then more bad news coming for a wave 5 top. Can you predict world events using chart patterns? Of course not, but when they work out you can remind everyone that you suggested it and look smart.

Charts of the Week

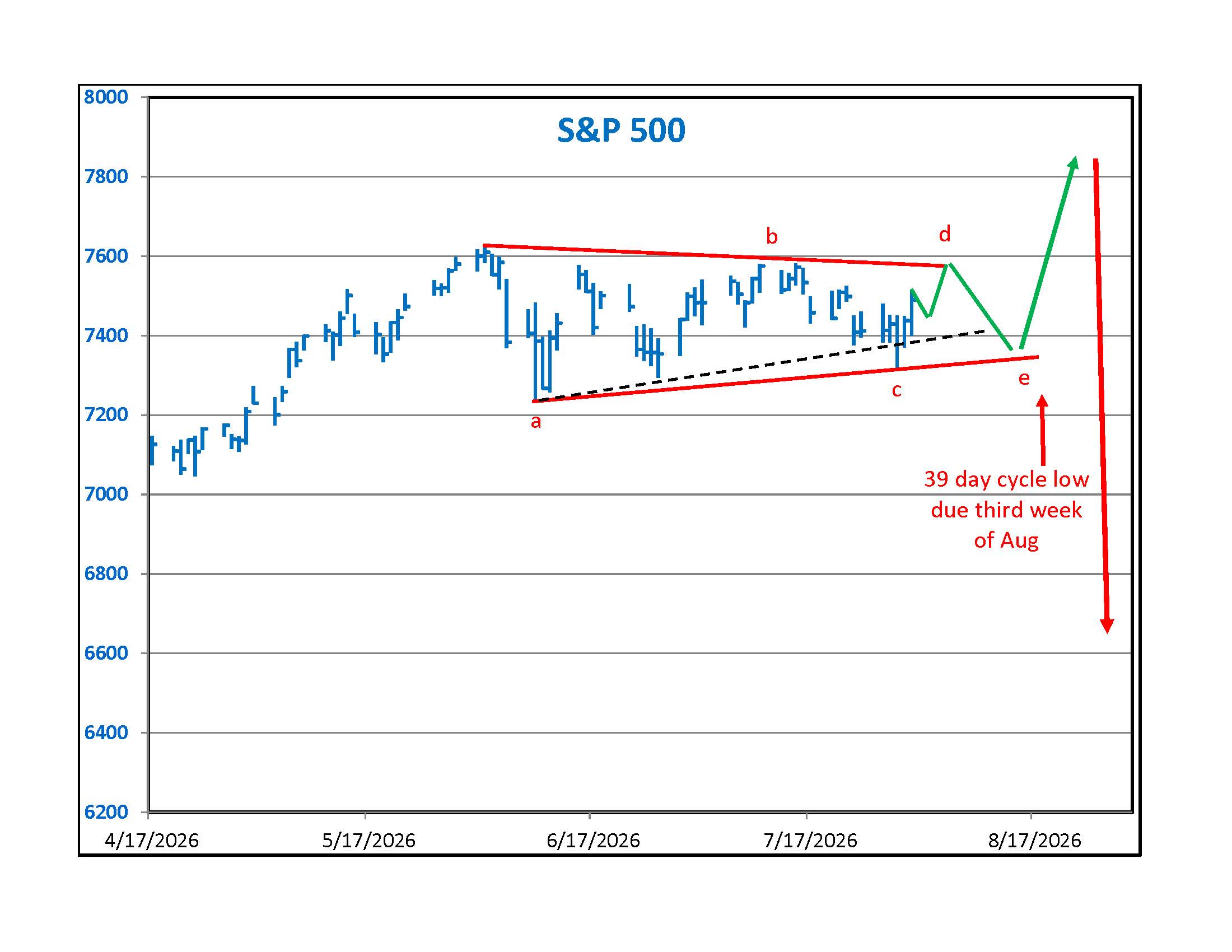

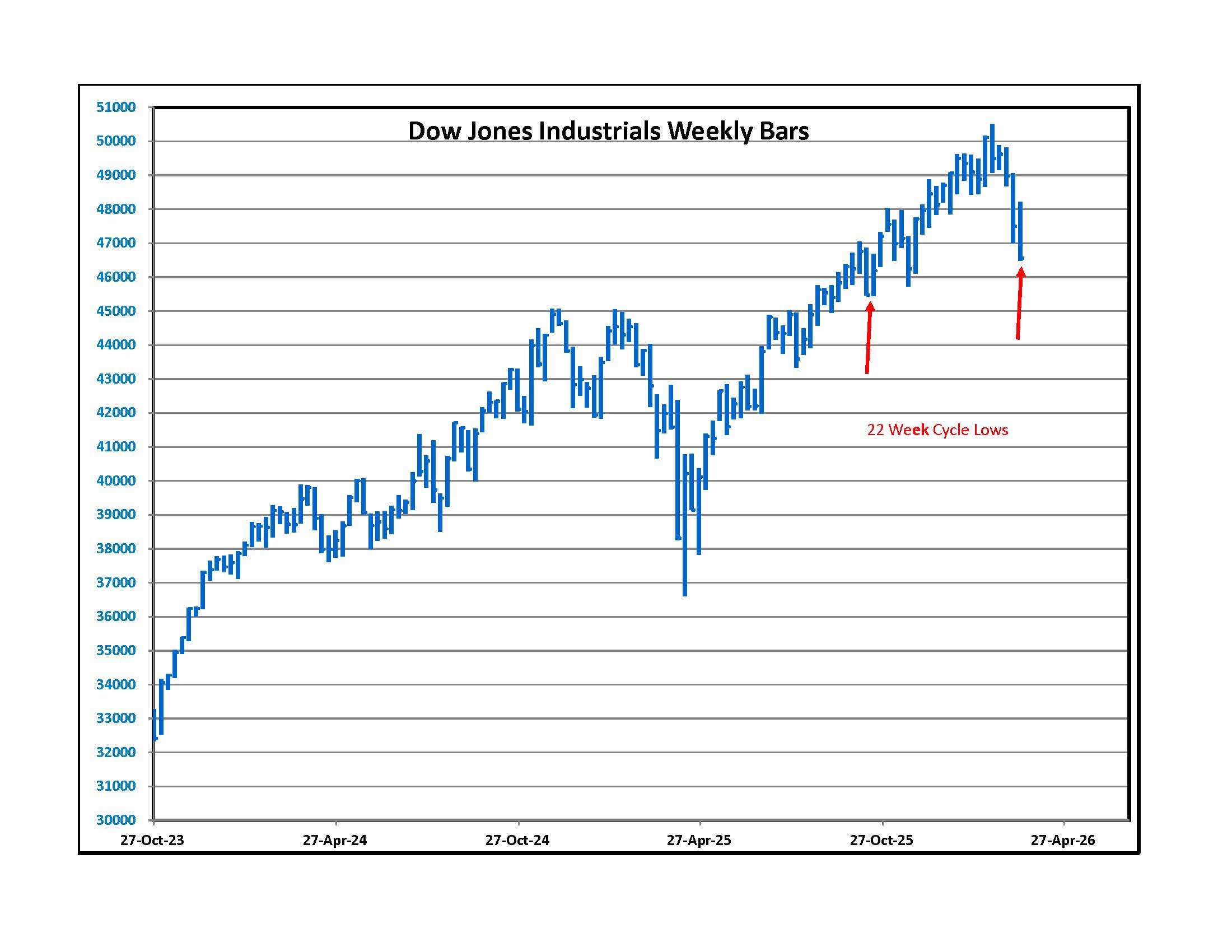

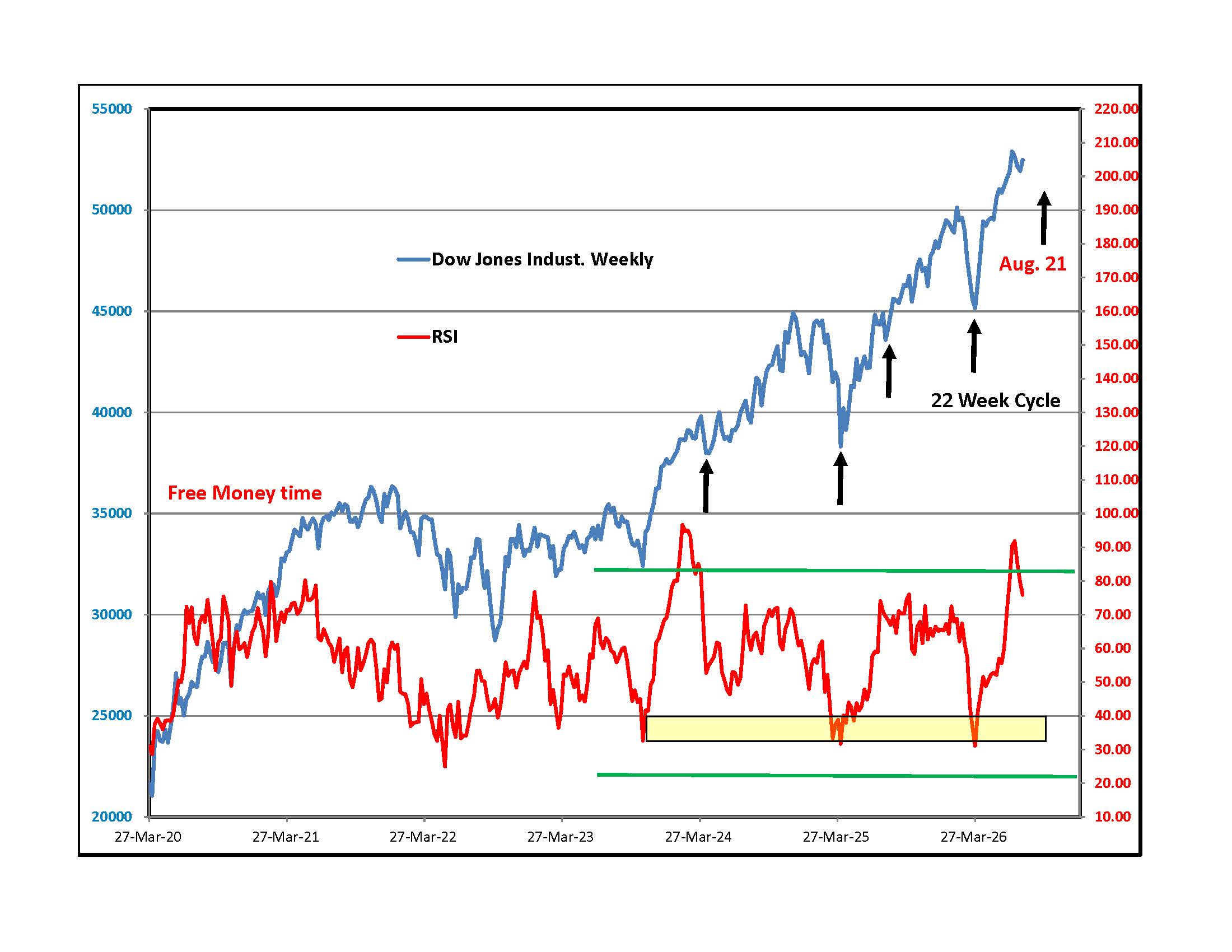

Two weeks ago the S&P looked like it was making a contracting pattern that would lead to a final thrust higher. The way I pictured it, a break of the dashed black line would invalidate the formation and lead to additional selling. Given the market action, it is also possible that the index is making the same kind of move but on a larger scale. If art rules over reality, we will get an up move towards the "d" point then a quick plunge towards "e" before a final thrust higher that sucks the last doubter into buying before a major reversal. Often, the sell off from "d" to "e" is driven by a negative headline. A break of last week's "c" point low will invalidate the pattern and be more immediately bearish. Frequent readers know I am a fan of Cyclesman.com's cycle low timing bands. One of his 39 day cycle lows is due around the third week of August. On the right is a weekly bar chart of the Dow Jones Industrials with red arrows pointing to Cyclesman.com's weekly timing bands. The next one is due around the same time period, the third week of August. These timing bands can run a bit long or short. They are seasonal indicators as opposed to pin-point timing tools.

On the left is a graph of the weekly closing price of the Dow Jones Industrial Average and a simple RSI graph in red. The RSI sat at .73 on Friday, a fairly high reading. On the right is daily bar chart of the same Average. The daily pattern of the Dow looks different from the S&P 500 and with the weekly RSI so high, we could get a larger sell off in the Dow than the S&P 500. The top four stocks in the Dow account for 30% of its weighting. They are Goldman Sachs at 11.52%, Caterpillar at 9.23%, Microsoft at 5.26% and United Health at 4.69%. Bad new on any of them could spark a down move that makes traders think that "the market" is selling off while the broader market suffers much less, similar to what we just saw with semiconductor stocks.

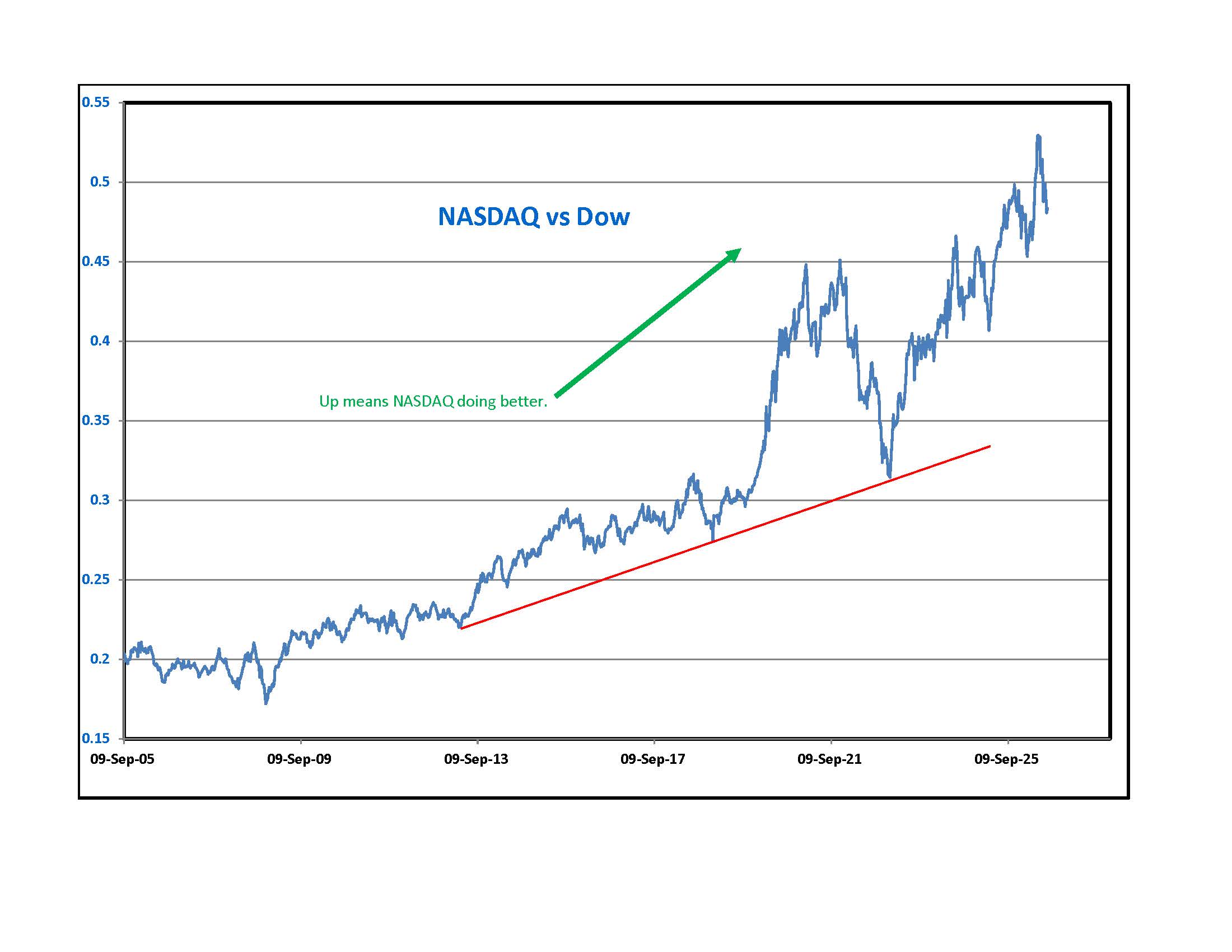

If my fantasy S&P 500 pattern works out, the final surge higher could be led by cyclicals, medium and small capitalization firms such as the ones included in the Russell 2000. Directly to the left is a line chart that tracks the relative performance of the Dow Industrials and the NASDAQ. Over time, tech is the clear winner but there are phases when non-tech catches up. If tech falters while other market averages advance, analysts will say that we are undergoing an investment rotation out of tech and into better performing segments of the economy. The reason this could lead to a final top is that 70% of capital expenditures come from AI investments. This money is spilling out into medium and smaller companies. If tech spending is peaking, the mid and small cap earnings will have a lag effect with earnings looking good for a couple of more quarters before turning down.

Note: Analysts often refer to "market rotation" to imply that you need to get out of the investments they sold you a year ago and switch to the new winners. Sometimes there are no new winners. Everything is selling off. Their use of "rotation" is a way to keep you in the market, generating commissions and fees.

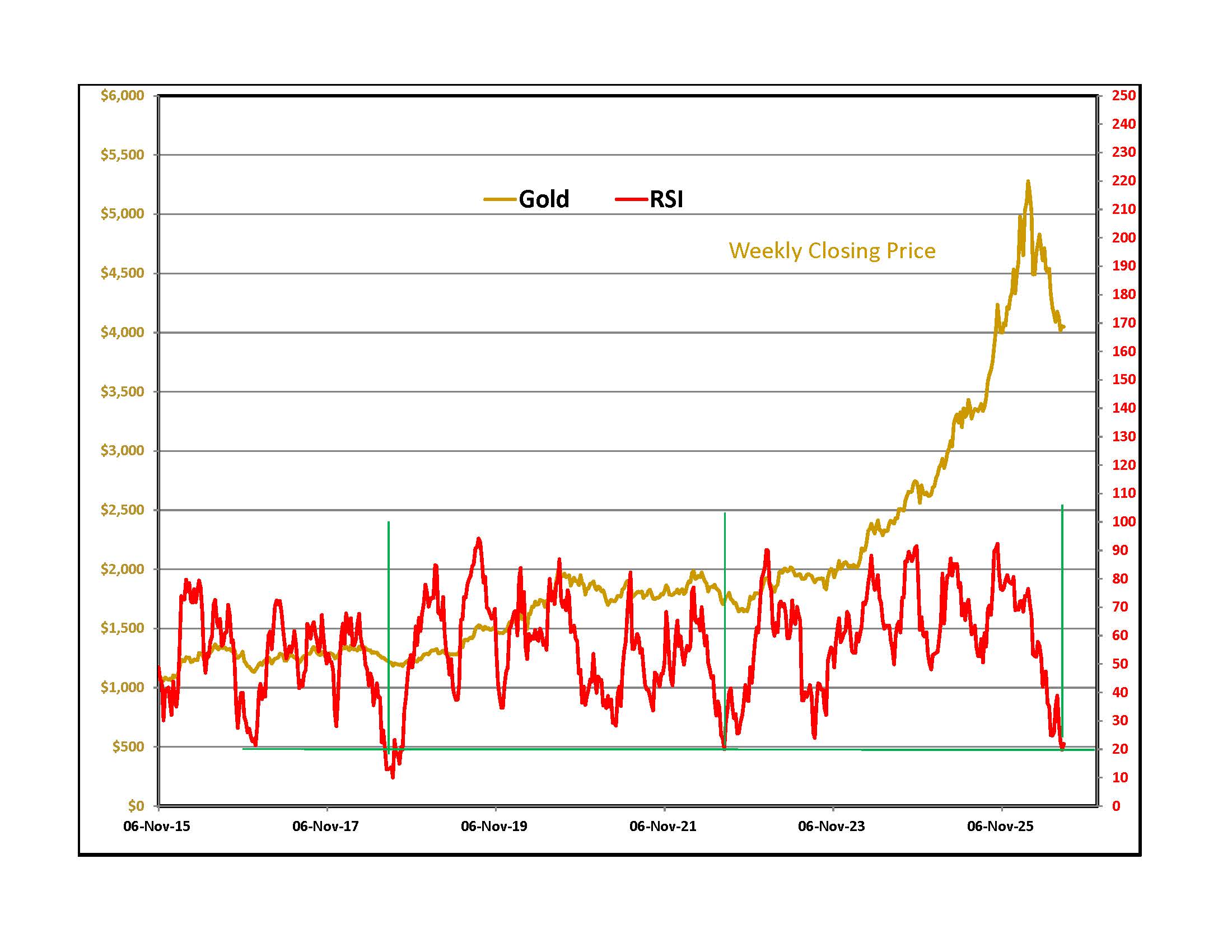

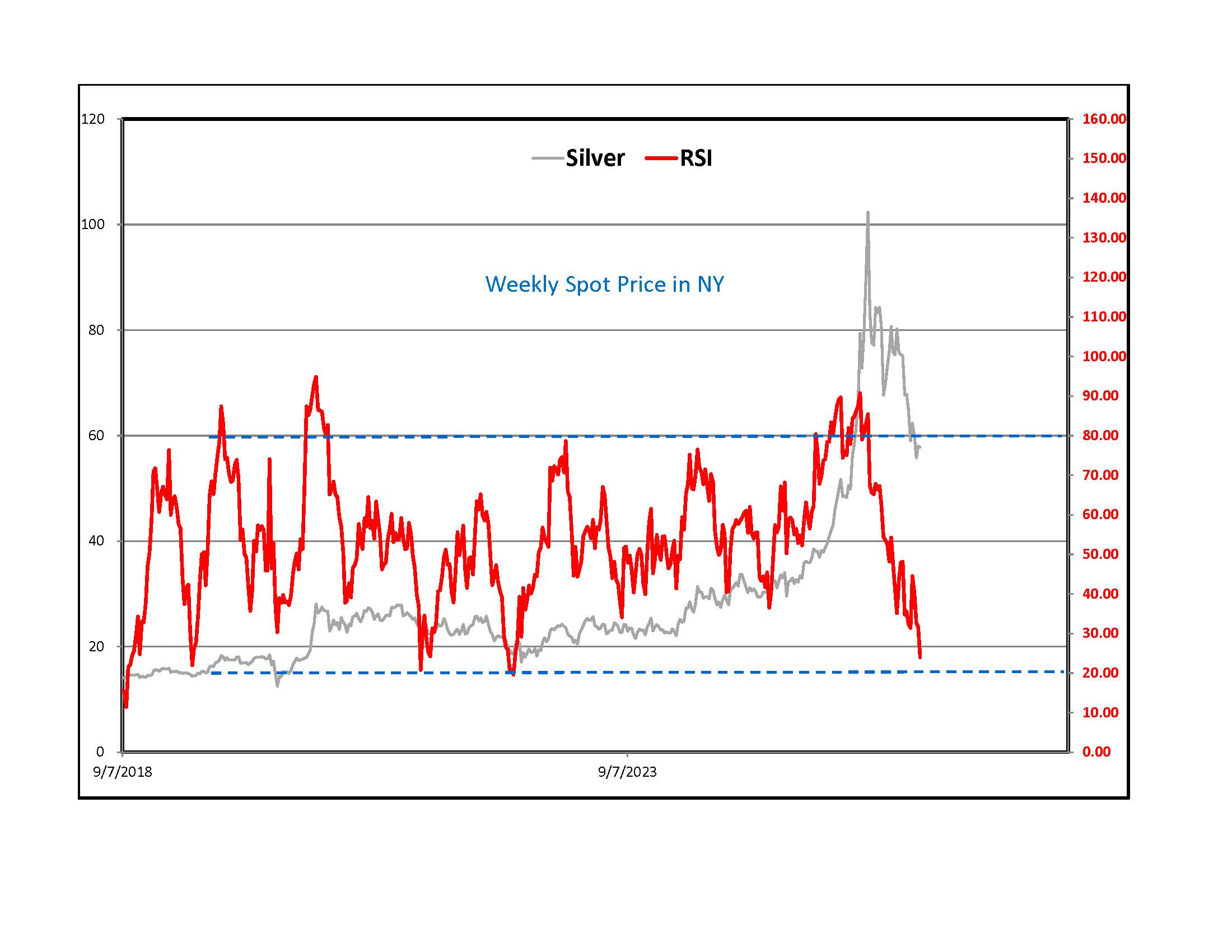

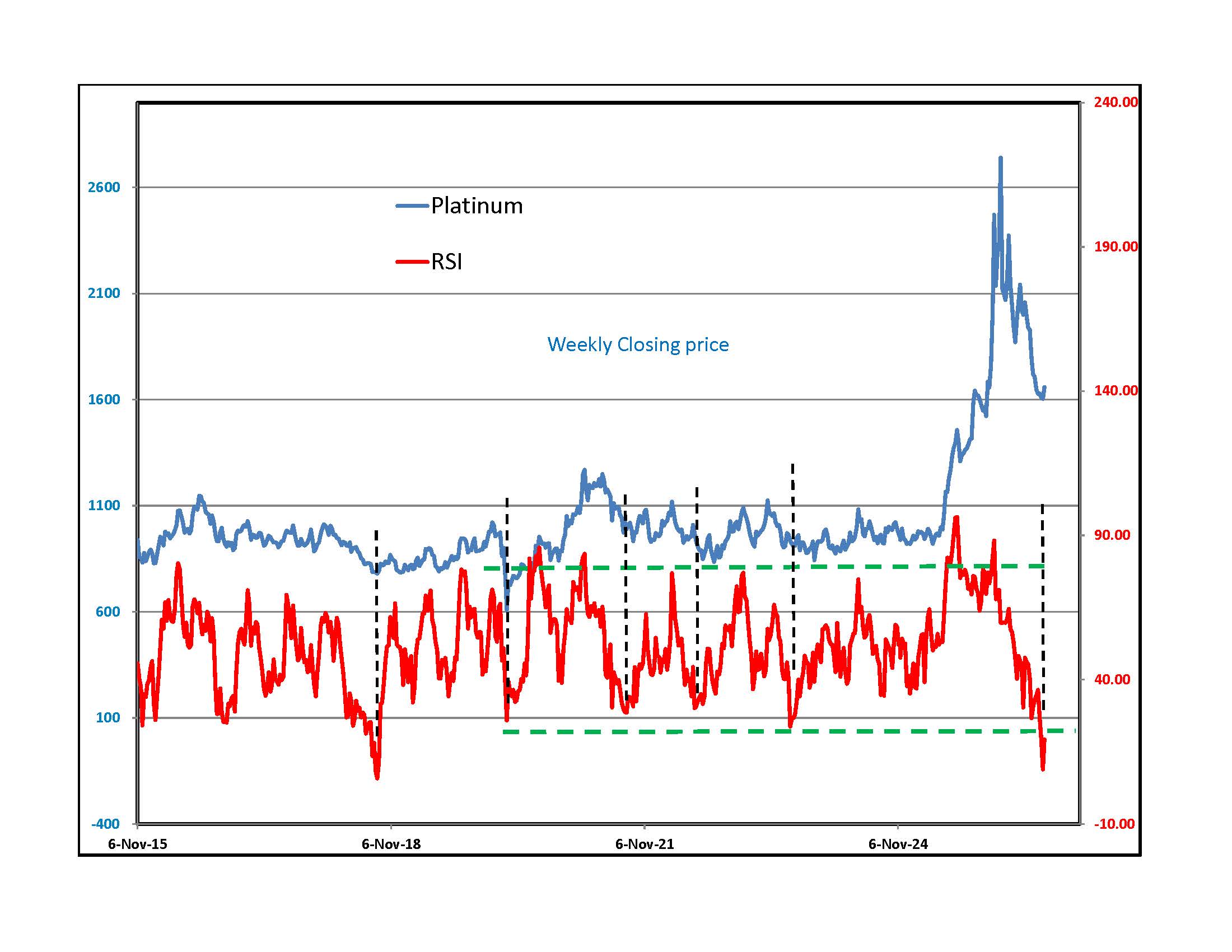

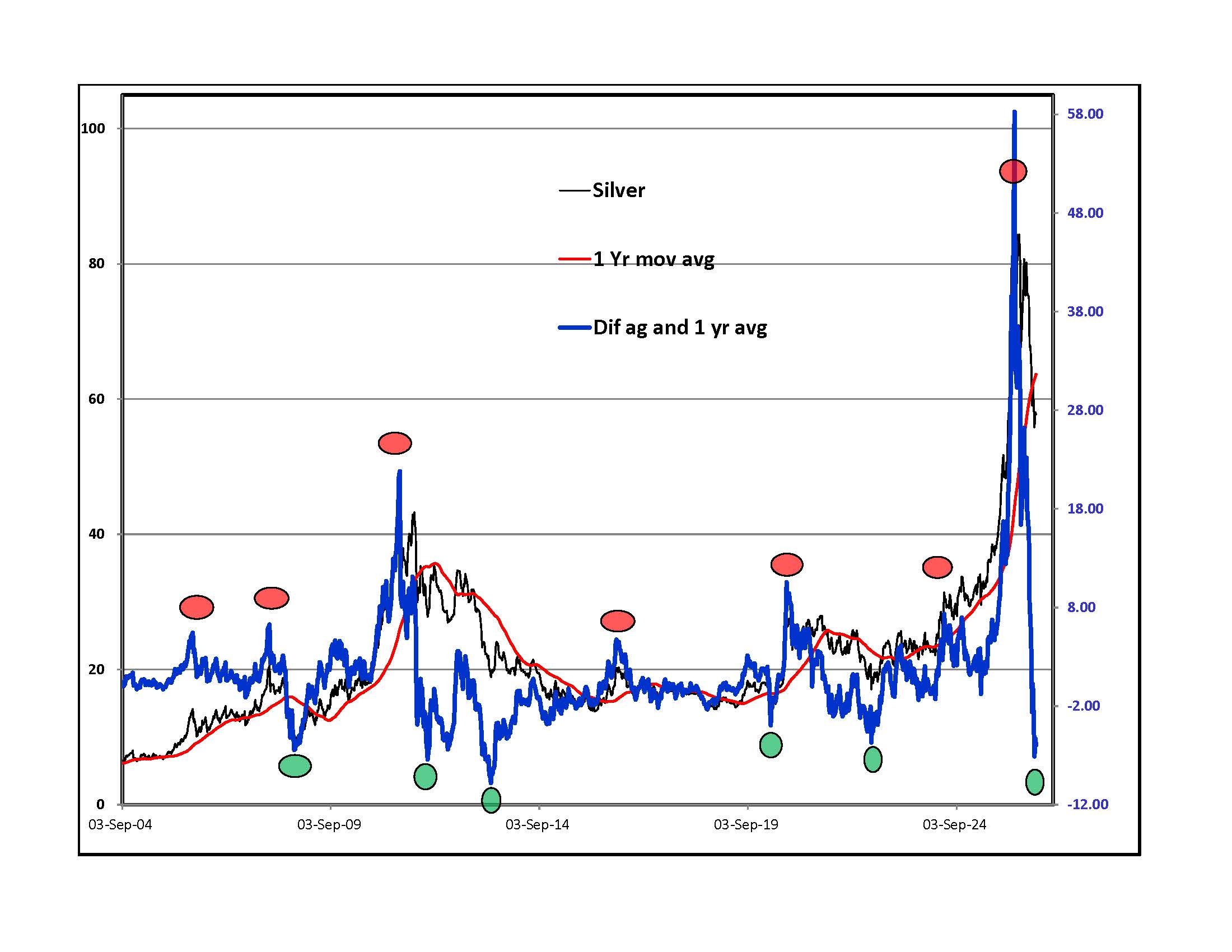

Last weekend I did an update focused on Gold and Silver featuring the graph of the weekly closing price of gold with a simple RSI oscillator (upper left) and silver with a line tracking the difference between its weekly close and one year moving average (lower right). This week I am adding a weekly silver close and simple RSI oscillator (upper right) and weekly platinum close along with an RSI line. Palladium usually goes in the same direction as platinum. All are in "over sold" territory. It is important to remember that in a real crash, things that are over sold continue to plunge. There are no guarantees. In recent past cycles, buying when these derivative markers were at the low end of their ranges proved to be a relatively low risk purchase. One more favorable thing is that we are in the middle of the timing band for one of Cyclesman.com's 18 week cycle low timing bands for gold. Warning: I am talking my book because I started trading junior gold and silver mining ETFs from the long side and own some going into this weekend.

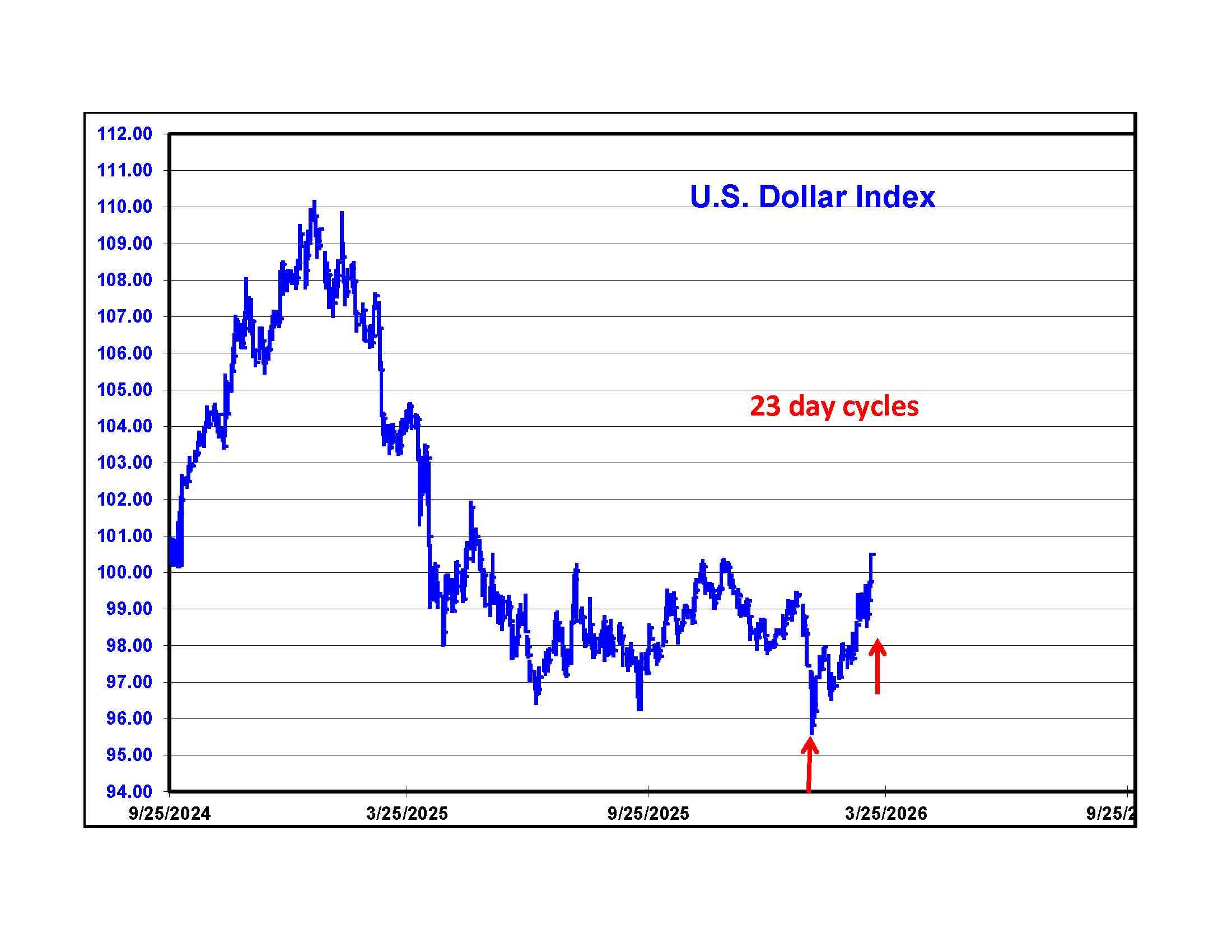

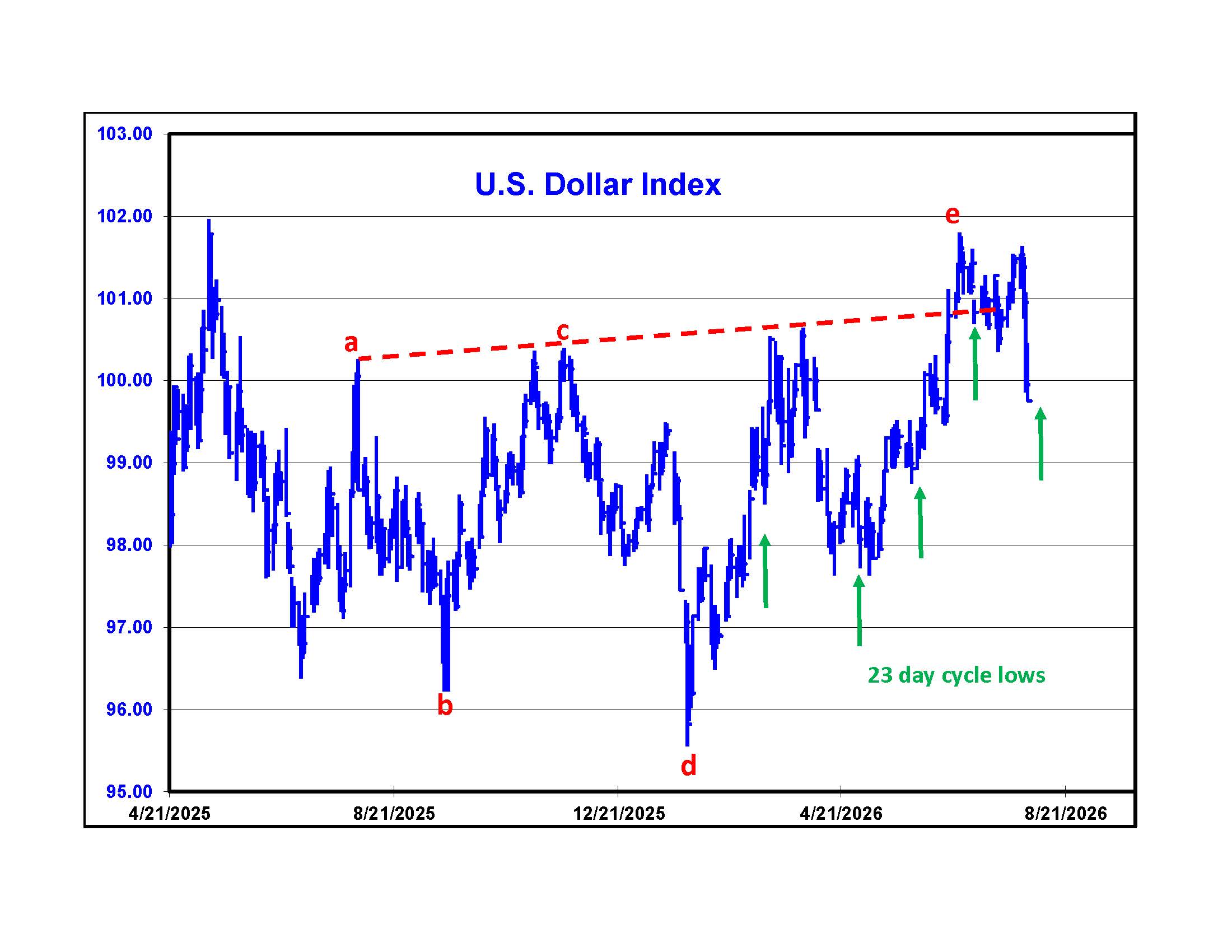

My fantasy Dollar pattern was that prices traced out an expanding triangle, labeled a,b,c,d,e and would sell off. Two weeks ago I didn't know what would make the Dollar go down but suspected it would have to do with the Yen, the second most heavily weighted currency against the Dollar in the index, behind the Euro. Last week, the Bank of Japan intervened in the market, selling Dollars and buying Yen. On Friday, our Treasury Secretary informed banks that the U.S. Treasury might also prop up the Yen against the Dollar. Speculators are not afraid of the Bank of Japan but they respect the Treasury. They covered Yen shorts against the Dollar, selling Dollars. Next week is the timing band for a 23 day cycle low so my theory will be tested coming into August.

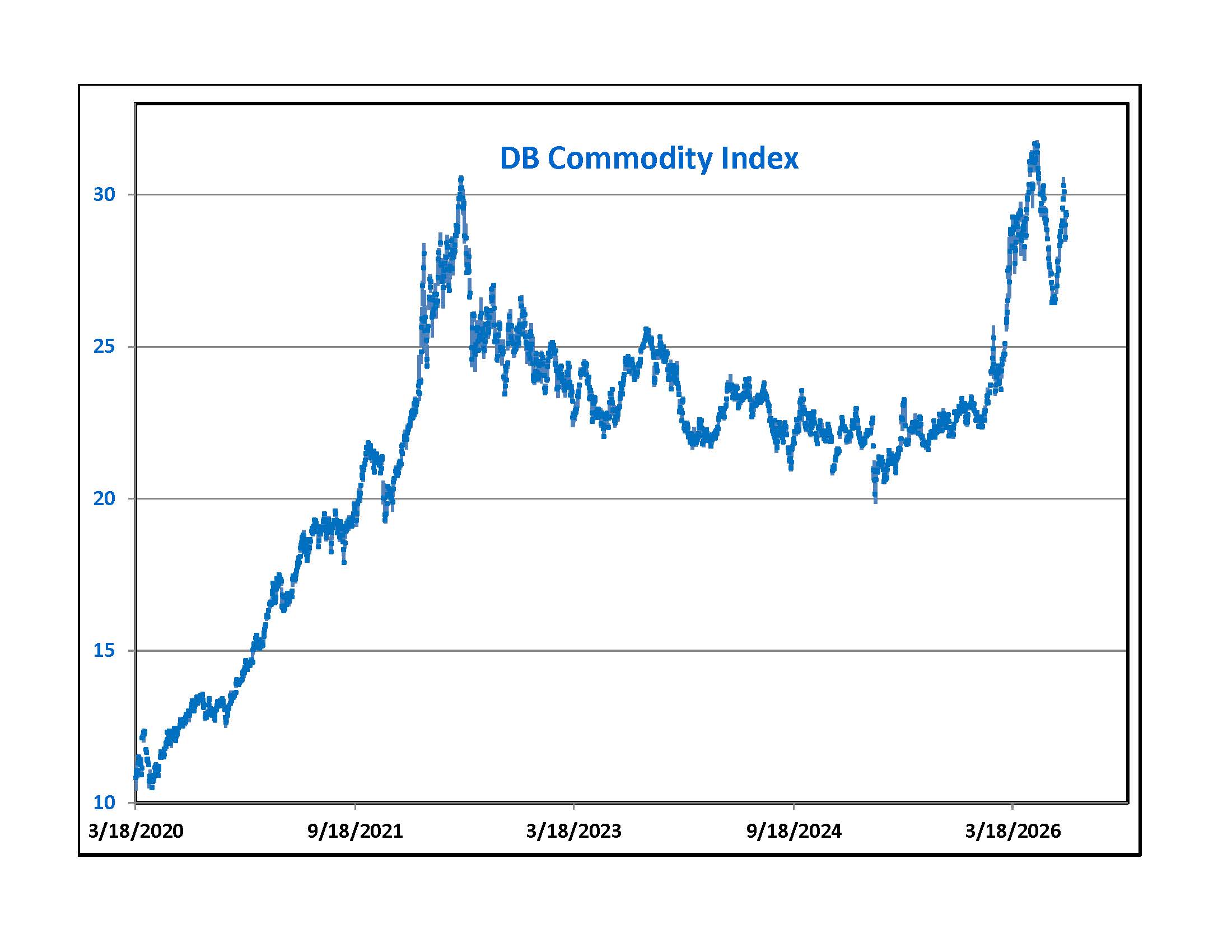

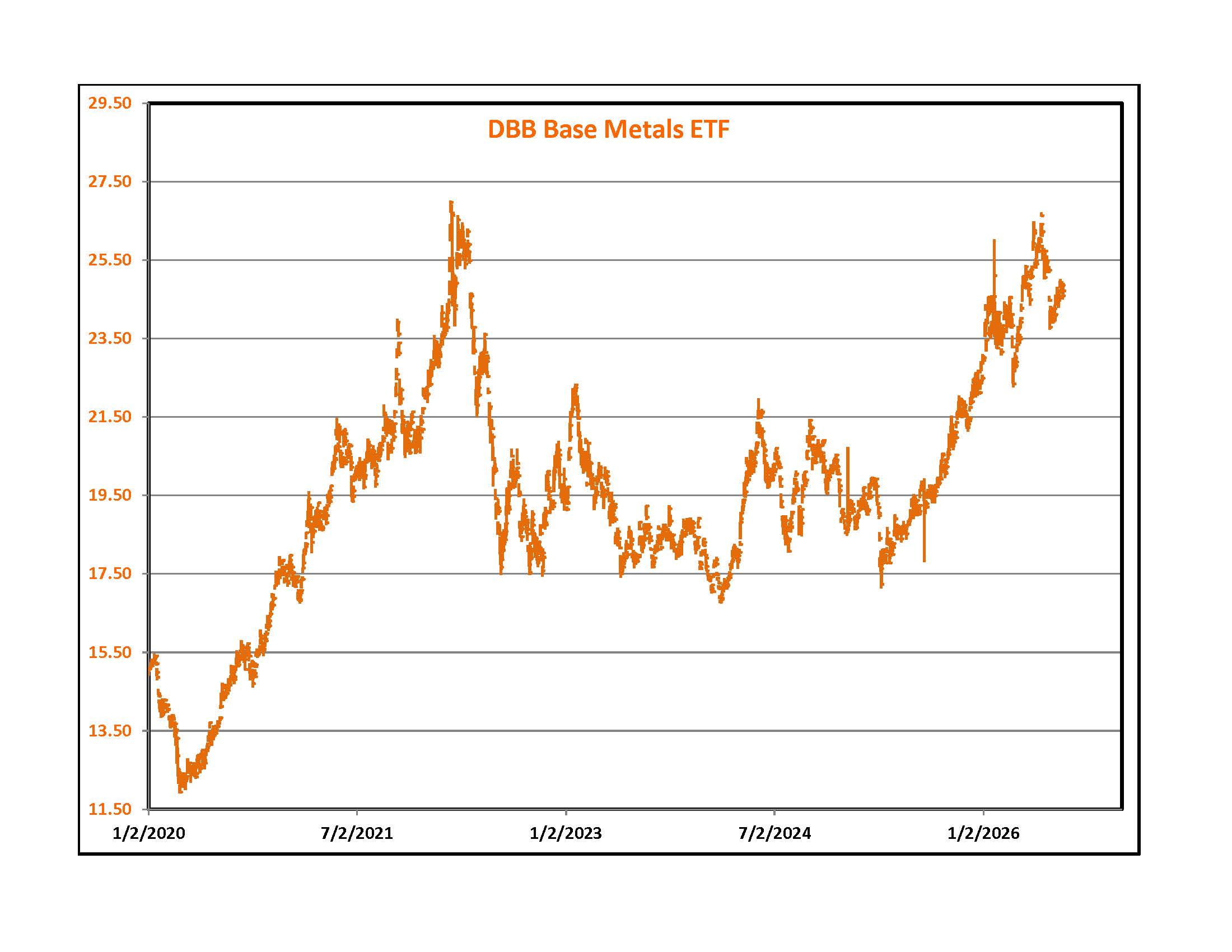

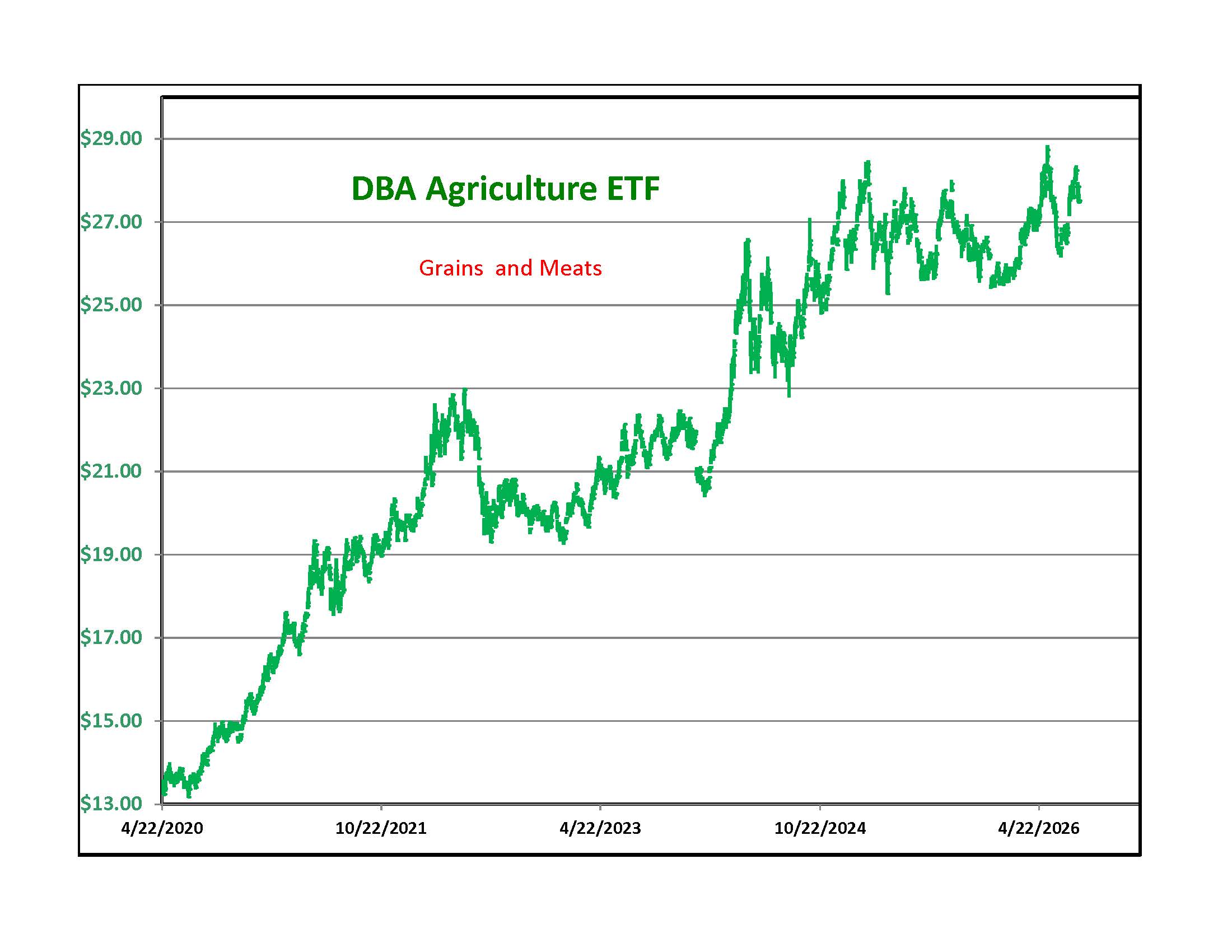

There is no shortage of investment podcasts on social media. There is a growing chorus of analysts warning about inflation due to supply constraints caused by the two wars and anticipated bad weather. The four graphs above focus on commodities. DBC tracks a basket of them, weighted a bit more toward crops than oil. DBB focuses on industrial metals. At the peak of an economic cycle, these tend to rise in price. DBA tracks grains and meats. Historical accounts of economic cycles usually include statistics on wheat prices as a proxy for the availability of food in general. So far, we have higher prices on all these graphs but no breakaway move to the upside. The population of working aged people who buy the most "stuff" is flat to declining in many parts of the world. During the 70s, the period most mentioned by inflation hawks, a huge baby boomer cohort was entering peak consumption and spending years so there was a natural increase in the demand for things and rising costs. If prices rise now, it will be because of supply problems, not demand. As regular readers know, wheat is my favorite. I own WEAT, an ETF that tracks wheat prices via nearby wheat futures. Last week, Russia sank a ship from Ukraine carrying corn. Analyst said that this was in response to Ukraine taking out Russia's imprtant money manking exports of oil, diesel and gasoline. Both countries are major exporters of wheat and use the Black Sea. Will they target wheat shipments next? Ukraine hit a Russian ship headed for Iran, claiming they were part of a regular weapons trade between the two countries. Will these two wars become interlinked with Iran also targeting agricultural exports from Ukraine? It looks worse by the week.

Best Guesses:

Stocks - I am going with the S&P chart mysticism that calls for a short rally to the upper trend line followed by a headline inspired quick down draft to the "e" and a final thrust to a high point this fall. You will know it is happening when your investment advisor tells you to get more aggressive and people in your office start being experts on the market.

Bonds - One of the reasons for last week's selloff could be Japan selling Treasuries for Dollars to support the Yen. Yields of 5.2% will look attractive to big institutions. Long term models of stock market valuation tell serious money that the upside is limited over time. Locking in something over 5% will not be a bad way to go. If short term rates stay low, there will be increased demand for longer dated yields of 5% or greater from players in the carry trade.

Gold and Silver - My weekly charts are saying that down side risk is limited at this point. I am biased because I own Jr. mining stock ETFs so beware.

Oil - Pure chart mysticism on XLE says things will get worse for a bit then better. Aside from that, the world is waiting to see what the U.S. does to Iran over the weekend and how they retaliate. Analysts are so fixated on the stock market that some are suggesting that President Trump wants to get this round over in time for Monday's morning bell at 9:30 NY time.

Other Commodities - If war spreads, it will be good for commodity prices. My worry is that our hyper-scalers may be at peak spending and how much more can governments spend? Populations of working people are shrinking or at least not growing. There might be supply constraints but where will the future demand come from?

As of Sunday morning, there are reports that there is some kind of new agreement in the Middle East that will open the Strait. President Trump called off attacks on Iran. It his holds going into Monday, expect all risk assets to open higher and energy related things to sell off.

Unneeded Commentary - Redistribution

The Democrat party was always in favor of redistribution. Now, the Democrat Socialists want to punish the rich and take their wealth to give to those that don't have as much. The U.S. income tax system is already very good at taxing the rich. The top 10% of tax payers pay 75%, more than the bottom 90% combined! The top one percent alone pay around 38%. Last week I saw a clip of Bernie Sanders villainizing Elon Musk, asking if it was right for one man to be wealthier than most of the rest of the country combined. I grew up in New England and followed Bernie Sanders for decades. He was always know as the kind of guy who wanted to be adored for his thoughts and feelings without working an honest day in his life. I read that when he was young, he was thrown out of a commune because he didn't do his assigned work. He has always been a guy who fought for the "working man" while avoiding anything that most of us would refer to as work. We all know guys like this. He used to rant and rave about millionaires but now that he is one of them (and owns 3 homes), he rants about billionaires. Elizabeth Warren (the fake Indian) is another one from my area who hates Elon Musk. She scammed the ethnic spoils system to land a job at Penn then Harvard. She owns a big house in a wealthy, all white section of Cambridge and is said to be worth between 7 and 9 million dollars. She is a one trick pony. Her game is to start by saying, "I am outraged - -." You can fill in the blank. This is accompanied by a shaking voice that lets you know she is so angry that she can hardly contain her rage and is close to tears. For some reason, older women in Massachusetts eat this up and keep voting for her. So, who is more of a redistributionist, Bernie Sanders, Elizabeth Warren or Elon Musk? Tesla, Elon Musk's company, employs around 136,000 people around the world. The average salary is approximately $89,000. In North America the average pay is around $100,000. SpaceX has "only" 14,200 employees with the average North American worker making $124,000. And then there is X, formerly Twitter. The head count is around 1,800 people with an average salary of $122,000 and typical bonus of $16,000. Neurolink is an Elon Musk company trying to use technology to bridge nerve injuries and help paralyzed people walk. It has around 469 employees with most of them in the U.S. Average pay is around $142,000 per year. If Bernie and Liz want to help people, where is their Neurolink? How many paychecks come from the offices and activities of Liz and Bernie? AOC and Bernie recently did an Oligarchy tour where they were spotted flying around the country in private jets! Elon Musk's employees all pay federal and state (were applicable) taxes. If they own homes, their Elon Musk generated compensation pays local real estate taxes. They buy things that have sales taxes attached, go to restuarants that support entry level jobs, pay gym memberships and hire people to maintain their houses.

SpaceX had a record setting IPO that raised 85.7 billion dollars. That money came from "the wealthy" who could afford to invest and it will be redistributed into salaries and payments to hundreds of other companies that will supply parts or services and have well compensated employees. SpaceX then sold an additional 90 billion dollars in bonds, volontarily taking money from "the wealthy" that will also go into goods and services supplied by companies with people getting paid. Our other tech "oligarchs" are also spending billions on data centers going into parts, sevices and people's wages.

For socialists, this kind of redistribution doesn't count because the recipients own products and skills that are in demand whereas most of the spokespeople and many members of the Democratic Socialist of America got their education in topics that don't have practical applications or job openings. They want to be loved and paid for their thoughts and feelings, like Bernie and Liz. They think it is unfair that someone who spent 4 years studying systematic oppression and other courses focusing on anger, resentment and blaming others, can't find a job while some shallow person who majored in chemical engineering can afford to spend weekends at the lake with their family.

So, who is more effective at redistributing wealth? Elon Musk or complainers like Bernie and Liz? What would be better for you town: A Democrat Socialist of America office with purple hair and nose rings or a Neurolink research facility?

Best of luck,

DBE